Key Highlights

- An HMRC compliance check is a review of your self-assessment tax return to ensure accuracy.

- Common triggers for a tax investigation include inconsistent figures, late submissions, and unexplained financial transactions.

- HMRC uses data analysis, checking bank statements and third-party information to flag potential issues.

- There are three main types of audits: full enquiry, aspect enquiry, and random checks.

- Keeping organised financial records is the best way to prepare for a potential HMRC tax investigation.

- Understanding the reasons for an audit can help you manage your tax return and avoid scrutiny.

Receiving a notice from HMRC about your self-assessment tax return can be a stressful experience for anyone. The thought of an audit might bring up worries and questions about your tax affairs.

However, an HMRC review doesn’t automatically mean you’ve done something wrong. It may simply be a routine compliance check.

This guide will walk you through the common reasons for a self-assessment audit, helping you understand what to expect and how to handle your tax return with confidence.

What Is a Self-Assessment Tax Return?

A Self Assessment tax return is how individuals and businesses in the UK report their income and pay the correct amount of tax to HMRC. Instead of tax being deducted automatically (as it is for most employees through PAYE), Self Assessment requires you to declare your income, expenses, and other financial details each year.

You’ll need to complete a Self Assessment if you’re:

- Self-employed as a sole trader earning more than £1,000 a year;

- A partner in a business partnership;

- A company director receiving untaxed income; or

- Someone earning income that isn’t taxed at source, for example, rental income, dividends, or capital gains.

When you file your return, you must report all sources of income, claim any allowable expenses, and calculate how much tax and National Insurance you owe.

HMRC then uses this information to confirm your final tax bill or issue a refund if you’ve overpaid.

What Is a Self Assessment Audit by HMRC?

A self-assessment audit, officially called a compliance check, is how HMRC verifies that the information on your tax return is correct and that you’ve paid the right amount of tax. It’s a structured review of your financial records.

An HMRC investigation isn’t necessarily a cause for concern. If your accounts are accurate and your records are in order, the process is often straightforward.

Knowing the types of audits and how to prepare for them can help you handle the situation calmly and professionally.

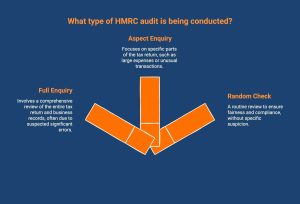

Types of Self-Assessment Audits

HMRC conducts several types of audits depending on what they need to verify and the level of risk identified in your tax return. Understanding these helps you respond appropriately if you’re ever selected for a review.

1. Full Enquiry

A full enquiry is the most detailed form of HMRC audit. It involves a thorough review of your entire Self Assessment tax return and all supporting financial records. These are usually triggered when HMRC believes there may be significant errors or risks in your reporting.

How to prepare:

- Gather all relevant financial records for the tax year, like bank statements, invoices, receipts, and expense records.

- Review your return for inconsistencies or missing information before HMRC raises them.

- Consider consulting an accountant or tax adviser to ensure everything is accurate and properly explained.

2. Aspect Enquiry

An aspect enquiry focuses on a specific area of your return, for example, a large expense claim, a sudden drop in income, or a transaction that seems unusual. These are narrower in scope and often resolved quickly if you can provide clear evidence.

How to prepare:

- Identify the section HMRC has queried and review the figures carefully.

- Gather supporting documents, such as receipts, contracts, or mileage logs.

- Provide concise, factual explanations to HMRC and avoid speculation or unnecessary details.

3. Random Check

A random check is a routine review selected without any sign of an error. Around 7% of audits fall into this category to ensure fairness and consistency across taxpayers.

How to prepare:

- Treat it as an opportunity to confirm your records are accurate and up to date.

- Make sure all your receipts and documentation match your return.

- Respond promptly and provide information within HMRC’s requested timeframe.

Which Taxes Can Come Under Scrutiny?

When HMRC carries out an audit, it may review several different taxes, not just your income tax. The areas checked depend on how your business operates, the type of income you earn, and whether you employ staff or are VAT-registered.

An audit aims to confirm that all your tax affairs comply with UK law and that everything reported to HMRC is accurate and complete.

Here’s how this typically works:

- Limited companies are usually reviewed for Corporation Tax compliance first.

- Businesses registered for VAT can have their VAT returns examined to verify sales and input tax claims.

- Employers may face a review of PAYE and National Insurance deductions to ensure employees’ tax has been correctly handled.

- Self-employed individuals or company directors can expect scrutiny of their Self Assessment tax returns.

- Individuals or businesses selling assets might be checked for accurate Capital Gains Tax reporting.

| Tax Type | Who It Affects | What HMRC Checks |

|---|---|---|

| Corporation Tax | Limited companies | Accuracy of profit reporting, business expenses, and deductions |

| VAT | Businesses registered for VAT | Correct calculation and payment of output and input VAT |

| PAYE & National Insurance | Businesses with employees | Proper employee tax deductions and employer contributions |

| Self Assessment | Sole traders, partners, and company directors | Income reporting, allowable expenses, and tax due |

| Capital Gains Tax | Individuals or businesses selling property, shares, or assets | Correct declaration of gains and reliefs claimed |

What Are The Common Reasons for HMRC Audit Self Assessment?

Most audits don’t just happen by chance. A small number are random, but the rest start because there is a red flag in your financial records. Let’s look at some of the most common reasons your assessment tax return may get a closer look.

1. Large or Unexplained Financial Transactions

Significant or irregular payments can draw HMRC’s attention, especially when they don’t align with declared income. Cash transactions are closely scrutinised, as they’re harder to verify.

HMRC may request bank statements to trace the source and purpose of large sums. Unexplained deposits or sudden income increases often lead to further checks.

2. Failure to Accurately Report Income

Omitting income, whether intentionally or by oversight, is one of the main triggers for HMRC audits. This could include undeclared rent, freelance work, or side income.

HMRC cross-checks your return with data from banks, the Land Registry, and other sources. If, for example, you own a property you don’t occupy, they may assume rental income unless stated otherwise.

3. Inconsistent or Incorrect Figures in Tax Returns

Inconsistencies between turnover, profit, or year-on-year figures raise immediate red flags. HMRC may open a review to confirm the reason behind large changes.

Always verify your figures before filing and keep supporting documents ready to explain any major variations in income or expenses.

4. Missing Deadlines on Self Assessment Submissions

Repeated late filings can suggest poor financial management and attract unwanted scrutiny. While one missed deadline results in a fine, ongoing delays increase the likelihood of an audit.

Filing early allows time for review, reduces errors, and demonstrates to HMRC that your tax affairs are well organised.

How Does HMRC Select Taxpayers for Review?

HMRC doesn’t review every Self Assessment return in detail. Most are processed automatically, but a small percentage are selected for closer examination. These checks can be random, but in most cases, HMRC’s decision is driven by data, like patterns, inconsistencies, or signals that suggest something may not add up.

Understanding what triggers a review helps you stay compliant and avoid unnecessary scrutiny.

1. Data-Driven Risk Assessment

HMRC uses a powerful data system to analyse information from multiple sources, including banks, employers, and government databases.

This software compares your declared income, expenses, and lifestyle indicators to identify inconsistencies. If the system spots missing income or claims that seem unusually high, your return may be flagged for further review.

2. Anomalies and Third-Party Reports

Significant changes in income or unusually large expense claims often raise red flags. HMRC also receives reports from third parties, such as financial institutions or other government bodies.

If external data doesn’t match what you’ve reported, your return could be selected for a compliance check.

3. Frequency of Audits

There’s no fixed schedule for HMRC reviews. Some businesses or individuals may be checked every few years, especially in high-risk industries or when returns show unusual patterns. Others may never be selected unless a potential issue is identified.

In essence, HMRC focuses on accuracy and consistency. Keeping complete records and ensuring your figures are correct gives them less reason to question your return.

How HMRC Uses Technology and Data Analysis in Audits?

HMRC does not just do manual checks anymore. Now, they use technology and simple data tools to help find tax returns that need a closer look. Let’s understand how this technology works.

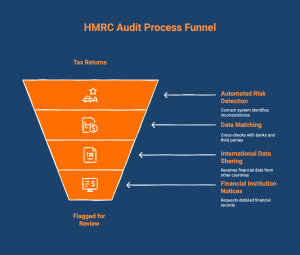

1. Automated Risk Detection with the ‘Connect’ System

HMRC no longer relies on manual checks alone. Its powerful data analysis tool, Connect, automatically identifies tax returns that may need closer inspection.

The Connect system analyses billions of data points from public, private, and international sources to build a detailed financial profile for every taxpayer. It compares your declared income and expenses with external data, such as property ownership, company records, and even social media activity.

If the system detects inconsistencies, such as high spending that doesn’t match declared income or unusually large expenses for your industry, your return may be flagged for review.

2. Data Matching with Banks and Third Parties

HMRC also cross-checks information from banks, building societies, and other financial institutions to confirm that all income has been declared accurately.

Each year, UK banks and building societies report the interest earned on savings accounts to HMRC, which is then compared with your tax return. Any missing or incorrect figures can trigger further investigation.

HMRC also receives financial data from other countries through international information-sharing agreements. This makes it difficult to conceal overseas income.

In some cases, HMRC can issue Financial Institution Notices requiring banks to provide detailed statements or transaction records about specific taxpayers under review.

What Happens During an HMRC Audit

Once your return is flagged, HMRC may begin a formal compliance check or audit. Understanding what to expect can make the process far less stressful.

a. Types of Contact

HMRC may reach out by letter, phone, or email to inform you of the audit and outline what they intend to review.

b. What HMRC Will Ask For

They’ll request documents such as tax returns, expense records, CIS statements, bank statements, and invoices to verify your reported figures.

c. Timeline of an Audit

Most audits take several weeks to a few months, depending on complexity. HMRC may pause the review while waiting for documents or explanations.

d. Communication and Cooperation

Respond promptly, provide all requested information, and keep communication polite and professional. Cooperating fully often helps resolve issues more quickly and can reduce potential penalties.

What Are the Key Self-Assessment Guidelines to Keep Your Accounts Audit-Ready?

Looking after your financial records is the best way for you to feel calm and ready if there is an audit. When your accounts are in order, it’s easier for you to file a self-assessment tax return.

Here’s how to keep your accounts accurate, audit-ready, and stress-free year-round.

1. Maintain a Consistent Bookkeeping Routine

Consistent bookkeeping is the foundation of audit readiness. Keeping your records up to date means you can provide accurate information straight away if HMRC requests it.

To stay audit-prepared:

- Set aside time each week to update your books.

- Scan and store receipts as soon as you receive them.

- Reconcile your accounts regularly to spot errors early.

A steady routine keeps your figures reliable and your audit trail clear.

2. Reconcile Bank Accounts Regularly

Regular bank reconciliation ensures your records match your bank statements, exactly what HMRC would check in an audit. It helps you detect issues before they become compliance risks.

In an audit situation:

- Reconcile your bank balance with your accounting records monthly.

- Keep copies of all statements and reconciliation reports.

- Record and explain any differences immediately.

When everything aligns, you can answer HMRC’s questions confidently and quickly.

3. Keep Receipts for Every Business Expense

Receipts are your evidence for every deduction you claim. Without them, HMRC could disallow expenses and increase your tax bill.

To maintain clear proof:

- Keep receipts for all business-related purchases.

- Digitise them straight away using a secure app.

- Categorise expenses correctly to match your tax return.

Accurate documentation strengthens your position and reduces audit pressure.

4. Review and Verify All Financial Entries

A simple review before submission can prevent costly HMRC enquiries. Small mistakes, such as transposed figures or missed income, often trigger unnecessary checks.

Before submitting your return:

- Double-check every entry and total for accuracy.

- Ask a qualified accountant or tax adviser to review your accounts.

- Use accounting software to flag manual errors.

Accurate, well-reviewed accounts show professionalism and readiness if HMRC ever investigates.

How Can Direct Payroll Help You Stay Audit-Ready and HMRC-Compliant?

Direct Payroll helps you stay on top of your taxes, self-assessment duties, and HMRC requirements without the stress. We make sure your payroll, CIS reporting, and records are accurate, complete, and ready if HMRC ever reviews them.

Our team takes care of everything from managing deductions and verifying details to filing returns correctly and on time. This means fewer errors, no missed deadlines, and full peace of mind knowing your business is always compliant.

With Direct Payroll, staying audit-ready feels simple, organised, and completely worry-free. Get in touch today to see how we can help your business stay compliant and confident.

Conclusion

Going through an HMRC self-assessment audit might feel tough, but knowing what could cause it helps a lot. Things like unclear money moves or small errors when you report what you earn are common reasons. Knowing these can be your best way to stay ready. The way you handle your money and keep your records matters. Doing things right and staying neat helps you avoid an audit and keeps your taxes in good order.

Frequently Asked Questions

Are self-employed individuals more likely to face an HMRC audit?

Self-employed individuals face higher audit chances since their income is self-reported. HMRC often targets cash-based or fluctuating-income professions, as these carry greater error and compliance risks in self-assessment submissions.

What happens if HMRC finds an error in my self-assessment tax return?

If HMRC finds an error, you must correct it and pay any tax due. Interest and penalties may apply, depending on the reason. In some cases, you could even receive a refund.

How can I avoid common triggers for an HMRC self-assessment audit?

Keep accurate records, declare all income, and file your return on time. Double-check for errors or inconsistencies. Organised, transparent financial documentation greatly reduces audit risks and ensures compliance confidence.

How do I Know If HMRC are investigating me?

HMRC will notify you officially by letter or occasionally by phone. The notice outlines the investigation’s reason and the information required for reviewing your tax affairs accurately.

Do HMRC Audit Self Assessment?

HMRC can audit self-assessment tax returns anytime to verify accuracy. They review declared income, expenses, and evidence to ensure figures align with your submitted financial records.

Do HMRC Do Self-Assessment Audit On Small Businesses?

HMRC frequently audits small businesses when figures appear inconsistent. They verify invoices, receipts, and deductions to ensure all declared income and expenses are reported truthfully.

When Do HMRC Do Self Assessment Audit?

HMRC carries out self-assessment audits either randomly or when its system flags unusual activity. This might include sudden income drops, missing information, or expense claims that don’t align with industry norms.

Do HMRC Check Bank Accounts?

HMRC can check bank accounts during a tax investigation or self-assessment audit. They compare your bank transactions with declared income to identify discrepancies, undeclared earnings, or suspicious financial activity that may require clarification.