TL;DR

|

|---|

Navigating automatic enrollment compliance can feel overwhelming for employers. With complex rules, tight deadlines, and rising regulatory scrutiny, failing to meet pension duties risks costly fines, damaged reputation, and unhappy employees. Many businesses struggle with keeping up-to-date, managing communications, and ensuring contributions, along with their PAYE reference, are paid on time.

This blog breaks down everything you need to know about auto-enrollment compliance, from your core responsibilities in the automatic enrolment process to the enforcement powers of The Pensions Regulator (TPR), common pitfalls, and upcoming legal changes. By following this guide, you’ll gain clarity and practical steps to confidently meet your obligations, avoid penalties, and build trust with your workforce.

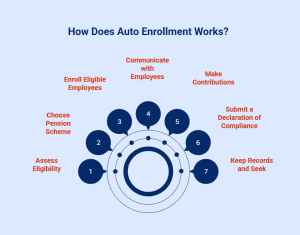

How Does Auto Enrollment Work for Businesses in the UK?

Auto enrollment requires UK employers to automatically enroll eligible employees into auto enrollment compliance schemes that meet legal standards. Here’s how businesses typically follow the process:

Step 1: Assess Eligibility

Determine which employees meet the age and earnings criteria set by law to qualify for automatic enrollment.

Step 2: Choose a Qualifying Pension Scheme

Select an appropriate auto enrollment compliance scheme, usually a Defined Contribution (DC) scheme, that meets government standards.

Step 3: Enroll Eligible Employees

Automatically enroll qualifying employees without requiring their consent. Employees may choose to opt out later if they wish.

Step 4: Communicate with Employees

Send written notifications explaining enrollment, rights to opt out, and other pension details within six weeks of the enrollment date.

Step 5: Make Contributions

Deduct pension contributions from employees’ pay and add the employer’s share. Ensure timely payment to the pension provider.

Step 6: Submit a Declaration of Compliance

File a pension auto enrollment declaration of compliance with The Pensions Regulator (TPR) by the deadline. This confirms that all duties have been met.

Step 7: Keep Records and Seek Help if Needed

Maintain accurate records of enrollment and contributions. Use resources such as HMRC Basic PAYE Tools (BPT) auto enrollment compliance help to stay updated on rules and ensure ongoing compliance.

By following these steps, UK businesses can fulfill their pension obligations efficiently, reducing risk and supporting employee financial security.

Check out our guide to PAYE Registration for employers.

Who Oversees Auto Enrollment Compliance?

The Pensions Regulator (TPR) is the official body responsible for ensuring employers meet their duties under the Pensions Act 2008, including enrolling eligible workers into a qualifying pension scheme and making contributions on time.

To enforce compliance, TPR can issue a range of notices and penalties, such as:

- Compliance Notices – Requiring employers to take corrective action quickly.

- Unpaid Contribution Notices – Demanding payment of missed contributions.

- Improvement Notices – Aimed at resolving specific ongoing issues.

- Fixed Penalty Notices – A flat £400 fine per breach.

- Escalating Penalty Notices – Daily fines from £50 to £10,000, depending on the business size.

Larger employers may receive heavier fines, particularly when employee contributions are withheld from salaries but not passed into the workplace pension.

To avoid these penalties, businesses should follow an auto enrollment compliance checklist, a step-by-step guide to ensure nothing is missed, from assessing worker eligibility to issuing employee communications and setting up contributions.

Some employers may also ask, “Is a work pension auto enrollment or salary sacrifice?” The answer is: auto enrollment is mandatory, while salary sacrifice is an optional arrangement that can be used to structure contributions more tax-efficiently. Both must still meet TPR’s compliance standards.

By staying informed and organised, businesses can protect themselves from enforcement actions and maintain trust with their workforce.

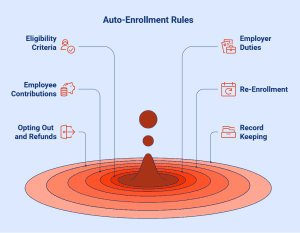

What Are the Rules for Auto-Enrollment?

Auto-enrollment is a legal requirement in the UK that ensures eligible workers are automatically enrolled into a workplace pension scheme. Employers must comply with specific rules set by The Pensions Regulator (TPR) to avoid penalties and support their employees’ retirement savings. Here are the key rules:

1. Eligibility Criteria

Employers must automatically enroll workers who:

- Are aged 22 to State Pension age

- Earn at least £10,000 per year (2024/25 threshold)

- Work in the UK

Even if employees don’t meet these criteria, they can still ask to opt into the scheme, and employers may need to contribute depending on their earnings.

2. Employer Duties

Employers must:

- Set up and maintain a qualifying workplace pension scheme, which is a key aspect of the employer’s responsibility.

- Assess employee eligibility regularly

- Automatically enroll eligible employees

- Contribute a minimum of 3% of qualifying earnings

- Send letters to employees explaining how auto-enrollment works and their rights

- Complete the declaration of compliance with TPR within five months of the staging/duties start date

3. Employee Contributions

Employees must contribute a minimum of 5%, bringing the total minimum contribution (including employer share) to 8% of qualifying earnings.

4. Re-Enrollment

Every three years, employers must reassess staff who opted out and re-enroll eligible ones. A new declaration of compliance is required after each cycle.

5. Opting Out and Refunds

Employees can opt out within one month of enrollment and receive a refund of any contributions made. After that, they can stop contributions but won’t be refunded.

6. Record Keeping

Employers must keep detailed records about pension contributions, communications, and assessments for at least six years.

What Legislative Updates Could Impact Employer Pension Duties?

Staying on top of legislative changes is essential for any employer looking to remain compliant with auto enrollment duties. Several proposed and upcoming updates could directly influence how businesses handle workplace pensions.

One of the most significant changes is the Pensions (Extension of Automatic Enrollment) Act 2023, which lays the groundwork for expanding the scope of auto enrollment in the coming years. This legislation allows for:

- Lowering the minimum age for auto enrolment from 22 to 18, potentially increasing the number of eligible employees.

- Scrapping the lower earnings threshold, meaning pension contributions would apply from the first pound earned, rather than starting above the current earnings trigger (£6,240 for 2024/25).

Although a firm auto enrollment compliance date for these changes has not been announced, the Department for Work and Pensions (DWP) has signalled that implementation could begin phasing in by the mid-2020s. These changes, once active, would raise employer responsibilities and potentially increase pension contribution costs.

To stay compliant, employers must ensure they can generate a timely and accurate auto enrollment compliance report, reflecting changes to eligibility, earnings calculations, and contributions.

Monitoring government bulletins, updates from The Pensions Regulator (TPR), and policy announcements is crucial to preparing in advance. Failing to adapt to new legal standards could lead to non-compliance and substantial penalties.

Are There Any Big Differences Between Auto-Enrollment Pension Providers?

Yes, there are significant differences between auto-enrollment pension providers in the UK. Employers should carefully compare providers before making a decision, as each one varies in fees, investment options, support services, and compliance features. Here’s a breakdown of the key differences:

1. Fees and Charges

- Some auto enrollment pension providers offer low or no setup fees but may charge on contributions and fund value.

- Others (auto-enrollment pension providers) may offer flat annual fees or tiered pricing based on the number of employees.

- Hidden costs, such as exit charges or admin fees, can also differ.

2. Ease of Integration

- Auto-enrollment pension providers usually offer payroll software integration for easier compliance.

- Some may support auto enrollment compliance reporting and reminders directly through their platform.

- Others may require more manual input, which increases administrative workload.

3. Investment Choices

- Most providers offer default funds, but some allow employees to choose from a range of investment options, including ethical or Sharia-compliant funds.

- The performance and risk level of default funds also vary across providers.

4. Employer and Employee Support

- Some providers give dedicated account managers or helplines, while others rely heavily on self-service portals.

- Auto-enrollment pension providers offer more detailed educational content and onboarding support.

5. Compliance and Reporting Tools

- Providers vary in how well they help with auto enrollment compliance.

- Some offer automated compliance date alerts, support for declaration submissions, and detailed compliance reports.

- Others may lack full visibility or automated tools for tracking employer duties.

6. Reputation and Scalability

- Established providers may offer more stability and trust, especially for growing companies.

- Some schemes are designed for microbusinesses, while others suit mid-sized and larger employers with customisation needs.

What is the minimum auto-enrolment contribution for 2025?

For the 2025/26 tax year (6 April 2025 to 5 April 2026), the minimum total contribution for auto-enrolment pensions in the UK remains 8% of qualifying earnings. This is split into:

- Employer contribution: at least 3% set rate

- Employee contribution: at least 5%, which includes tax relief

Qualifying earnings are defined as the portion of an employee’s earnings between the lower earnings limit (LEL) and the upper earnings limit (UEL). For the 2025/26 tax year, these thresholds are:

- LEL: £6,240 per year

- UEL: £50,270 per year

This means that contributions are calculated on earnings between £6,240 and £50,270. Earnings below £6,240 are not considered for contribution calculations.

Employers may choose to base contributions on different definitions of earnings, such as basic pay or total pay, provided they meet the statutory minimum contribution requirements. However, the standard approach is to use qualifying earnings as defined above.

It’s important to note that these thresholds and contribution rates are subject to annual reviews by the government and may change in future tax years.

What Risks Do Employers Face with Non-Compliance?

Non-compliance with automatic enrollment duties can expose employers to serious risks, financial, legal, and reputational. Failing to meet legal duties can trigger escalating penalties, additional interest, and even the requirement to pay missed contributions on behalf of both the business and employees.

For instance, if contributions are overdue by more than three months, there may be very little time before TPR can order employers to cover the full amount, including employees’ shares. Beyond fines, companies risk criminal prosecution for willful breaches, with the possibility of imprisonment for senior officers.

Employers might also face claims from employees if their pension rights are violated, leading to time-consuming disputes and tribunal hearings. “What risks do employers face with non-compliance?” The answer: significant financial consequences, operational disruption, and long-term damage to trust and brand reputation within the workforce and wider market.

How Direct Payroll Simplifies Payroll and Auto Enrolment Compliance?

Direct Payroll Services makes payroll and auto enrollment compliance easy for UK businesses. They handle accurate payroll processing, pension assessments, contribution deductions, and compliance reporting, ensuring you meet all deadlines without hassle.

With expert support and up-to-date technology, they reduce your admin burden and help avoid penalties, so you can focus on running your business confidently. Contact us today.

Conclusion

Automatic enrollment compliance is not just a regulatory obligation but a crucial aspect of responsible business management, including the client’s declaration of compliance. As the landscape of pension duties continues to evolve, it is essential for employers to stay informed and proactive in their compliance strategies.

Understanding the implications of non-compliance, including potential penalties and reputational risks, underscores the need for vigilance in this area. By implementing robust systems and regularly reviewing practices, businesses can navigate the complexities of auto enrollment effectively. If you’re seeking guidance on how to ensure your business is compliant, don’t hesitate to reach out for expert advice.

Frequently Asked Questions

1. What happens if an employee opts out after automatic enrollment?

If an employee opts out after automatic enrollment, their pension contributions stop, and they lose employer contributions. However, they can rejoin the private pension scheme in the future. Employers must inform employees about their rights regarding opting out and the auto-enrollment process.

2. How often must employers re-enroll employees who previously opted out?

Employers must re-enroll eligible jobholders who previously opted out every three years. This re-enrollment process ensures that eligible employees are given another opportunity to participate in the pension scheme, aligning with automatic enrollment regulations and helping maintain compliance.

3. Can temporary or part-time workers be automatically enrolled?

Yes, temporary or part-time workers can be automatically enrolled in pension schemes if they meet specific criteria, such as age and the annual earnings trigger for auto-enrollment and earnings thresholds. Employers must regularly assess these workers to ensure compliance with auto-enrollment requirements and avoid potential penalties.

4. How does salary sacrifice affect pension auto enrollment contributions?

Salary sacrifice agreements involve an employee reducing their gross earnings, with the employer paying the equivalent pension contributions directly. This can increase tax relief and lower employer National Insurance costs. Employer contributions through the PAYE scheme must still meet the minimum required for pension auto enrollment.

5. What should employers do if they discover an error in pension contributions?

If employers discover an error in pension contributions, they must promptly investigate the issue. Correct any inaccuracies and notify employees affected. It’s also essential to inform pension providers and consider rectifying payments, ensuring compliance with regulatory requirements to avoid potential penalties.

6. Which employers are exempt from auto-enrolment?

Employers with no eligible jobholders (for example, all staff are under 22, over State Pension Age, or earn below the £10,000 threshold) are exempt from auto-enrolment duties.

7. Is auto-enrolment or salary sacrifice?

Auto-enrolment is a legal requirement to provide a workplace pension, while salary sacrifice is an optional arrangement where employees exchange part of their salary for pension contributions, often giving tax and NI savings.