Key Highlights

- Benefits in kind are non-cash perks provided by employers that carry a taxable value.

- Most benefits are taxed as part of an employee’s income based on HMRC valuation rules.

- The tax applied depends on the employee’s income tax band, not the type of benefit.

- Employers must report benefits through payroll or P11D and pay Class 1A National Insurance.

- Incorrect valuation or reporting can lead to penalties and payroll discrepancies.

- Payrolling benefits simplifies tax collection and improve transparency.

- A structured process ensures accurate reporting and compliance with HMRC requirements.

Benefits in kind tax applies when employees receive non-cash perks such as company cars, private healthcare, or accommodation. These benefits are treated as taxable income, which means they must be correctly valued and either included in payroll or reported to HMRC.

The complexity comes from how each benefit is assessed and taxed. Different rules apply depending on the type of perk, and incorrect valuation or reporting can affect PAYE calculations, employee tax positions, and overall compliance. With changes such as mandatory payrolling of benefits approaching, accurate handling is becoming more important for businesses.

This guide explains how benefits in kind tax works in the UK, how it is calculated, and what employers need to do to report it correctly. It also outlines how these benefits impact employees and how payroll processes can be managed to reduce errors and maintain compliance.

What Is Benefits in Kind Tax in the UK?

Benefits in Kind (BIKs) are non-cash benefits provided by an employer that are treated as taxable income in the UK. In simple terms, if you receive a benefit instead of money, such as a company car or private health insurance, you still pay tax on its value. HMRC calculates how much that benefit is worth and adds it to your taxable income.

The tax is then applied through payroll or self-assessment, depending on how the benefit is reported. Employers are also responsible for reporting these benefits and paying any required National Insurance contributions. In practice, Benefits-in-kind tax ensures that non-cash perks are taxed in the same way as salary, maintaining fairness across different types of compensation.

What Are The Common Types of Benefits In Kind?

Benefits in kind cover a wide range of non-cash perks provided by employers. These typically include company cars, private healthcare, accommodation, and subsidised meals, along with other benefits such as low-interest loans or childcare support. Each type is assessed separately, with specific rules used to determine its taxable value.

Each of these benefits is taxed differently, depending on how its value is calculated and reported to HMRC. The sections below explain how the most common benefits in kind are assessed and taxed in practice. practice.

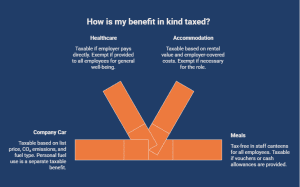

1. How Are Company Cars Taxed?

A company car used for personal travel, including commuting, is treated as a taxable benefit. The taxable value is calculated using the vehicle’s list price, CO₂ emissions, and fuel type.

Higher-emission vehicles generally result in a higher taxable value, while lower-emission or electric cars attract reduced rates. If fuel is also provided for personal use, it is treated as a separate taxable benefit, increasing the total tax liability.

2. What About Healthcare And Wellbeing Perks?

Healthcare-related benefits are usually taxable when the employer pays for them directly. This includes private medical insurance or health cover arranged on the employee’s behalf.

Some services are exempt when they are provided to all employees and relate to general well-being. These can include health screenings or counselling services. In contrast, benefits such as employer-funded gym memberships are typically treated as taxable.

3. How Are Accommodations Taxed?

Employer-provided accommodation is generally taxable. The value is based on the property’s rental value and any additional costs covered by the employer, such as utilities. If the employee contributes towards the accommodation, this reduces the taxable value.

In limited cases, accommodation may be exempt where it is necessary for the role, such as where living on-site is required to perform job duties.

4. How Are Meals Treated?

Meals provided in a staff canteen available to all employees are usually tax-free. This applies where the benefit is broadly accessible and not linked to individual compensation. However, meal vouchers or cash allowances are treated as taxable income because they have a direct monetary value.

Meals provided for specific business purposes, such as working late, may also qualify for exemption depending on the circumstances.

What are the Differences Between Cash Benefits and Benefits in Kind?

Cash benefits, such as salary or bonuses, are paid directly and taxed through PAYE with National Insurance. The value is clear and can be used freely. Benefits in kind are non-cash perks with a monetary value, such as company cars or private health insurance. HMRC assigns a value to these benefits, which is then added to taxable income.

This distinction matters in payroll because incorrect classification can lead to underpaid tax, reporting errors, and compliance issues with HMRC.

| Feature | Cash Benefits | Benefits in Kind (BIKs) |

|---|---|---|

| Definition | Direct cash payment | Non-cash perks with value |

| Taxation | Taxed via PAYE | Taxed on assigned value |

| Flexibility | Fully flexible | Fixed benefit |

| Reporting | Automatic in payroll | P11D or payrolling |

Correct classification ensures that both tax deductions and reporting obligations are handled accurately, reducing the risk of payroll discrepancies and penalties.

How Does Benefits in Kind Tax Work?

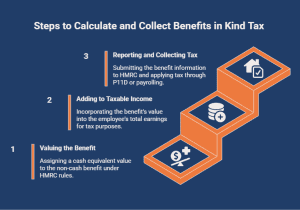

Benefits in kind tax is applied through a structured process that ensures non-cash benefits are correctly valued, reported, and taxed alongside salary.

The process involves three key stages, each affecting how tax is calculated and collected.

1. Valuing the Benefit

Each benefit is assigned a cash equivalent value under HMRC rules. This value reflects what the benefit is worth, not what it costs the employer.

This step determines how much of the benefit will be subject to tax.

2. Adding the Value to Taxable Income

The calculated value is added to the employee’s total earnings for tax purposes. This increases the overall taxable income for the year. As a result, employees may pay more tax or move into a higher tax band depending on the value of the benefit.

3. Reporting and Collecting Tax

Employers report benefits either through P11D forms or by including them in payroll.

- P11D method: HMRC adjusts the employee’s tax code after the tax year

- Payrolling: Tax is applied in real time through monthly pay

The reporting method determines when and how tax is collected. In practice, benefits-in-kind tax works by converting non-cash perks into taxable value, then integrating them into payroll so that tax is applied consistently with other earnings.

What Tax Rates Does HMRC Apply to Benefits In Kind?

Once the cash-equivalent value of a benefit is calculated, it is added to the employee’s total taxable income. The benefit is not taxed at a separate rate; instead, it is taxed at the employee’s standard income tax rate based on their tax band.

This means the value is taxed at 20% for basic-rate taxpayers, 40% for higher-rate taxpayers, or 45% for additional-rate taxpayers. The rate applied depends on total annual income, not on the type of benefit provided.

In addition to employee tax, according to the Government Report, employers must pay Class 1A National Insurance Contributions (NICs) on most taxable benefits. This is typically charged at 15% of the benefit’s value, although rates can change depending on the tax year

What Are Tax-Free Benefits in Kind?

Not all benefits in kind are subject to tax. HMRC allows certain benefits to be provided without increasing an employee’s taxable income, subject to specific conditions. These exemptions are designed to support employee welfare or cover minor perks without creating additional tax liability.

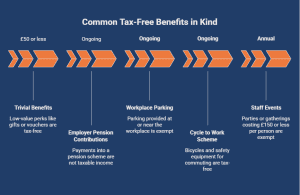

The most common tax-free benefits include:

- Trivial benefits: Low-value perks costing £50 or less, provided they are not cash, not linked to performance, and not part of contractual pay. Examples include small gifts, vouchers, or seasonal items. Directors of close companies are subject to an annual £300 limit.

- Employer pension contributions: Payments made by an employer into a pension scheme are not treated as taxable income for the employee.

- Workplace parking: Parking provided at or near the workplace is exempt from tax.

- Cycle to Work scheme: Bicycles and safety equipment provided under approved schemes are tax-free when used for commuting.

- Staff events: Annual events, such as parties or gatherings, are exempt if the cost per person does not exceed £150 per year.

These exemptions matter in payroll because correctly identifying tax-free benefits prevents unnecessary tax deductions and ensures accurate reporting to HMRC.

In practice, applying these rules allows employers to provide additional value without increasing tax exposure, while ensuring compliance with payroll and tax regulations.

How Is Benefit in Kind Tax Calculated?

Benefit-in-kind tax is calculated by determining the taxable value of a non-cash benefit and applying the employee’s income tax rate. HMRC sets specific rules for valuing each type of benefit to ensure consistent calculation.

- Basic formula: Taxable value × income tax rate = tax payable

- Example: A benefit valued at £2,000 taxed at 20% results in £400 annual tax

- Key factors affecting the calculation:

- The employee’s income tax band

- The valuation method for the specific benefit (e.g., company cars, insurance)

- Any employee contribution that reduces the taxable value

The accuracy of the calculation depends on the correct valuation and the employee’s applicable tax rate.

What Steps Should Employers Follow to Manage Benefits in Kind?

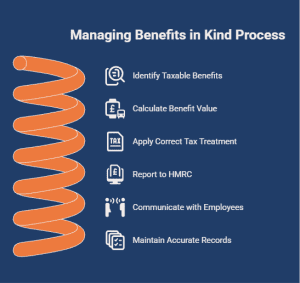

Managing benefits in kind requires a structured process to ensure accurate calculation, reporting, and compliance with HMRC requirements.

- Step 1: Identify taxable benefits: Review all employee perks and determine which are taxable and which are exempt.

- Step 2: Calculate the benefit value: Apply HMRC rules to assign a cash-equivalent value to each taxable benefit.

- Step 3: Apply correct tax treatment: Ensure the benefit is taxed correctly for employees and account for Class 1A National Insurance contributions.

- Step 4: Report to HMRC: Submit benefit details through payrolling or via P11D and P11D(b) forms within the required deadlines.

- Step 5: Communicate with employees: Explain the value of benefits and how tax is applied to avoid confusion.

- Step 6: Maintain accurate records: Keep detailed documentation of benefits, calculations, and submissions for compliance purposes.

Following these steps ensures consistent reporting, accurate tax handling, and full compliance with HMRC requirements.

What Happens If Benefits in Kind Tax Is Reported Incorrectly?

Incorrect reporting of benefits in kind can lead to financial and compliance issues for both employers and employees.

- Employer penalties: HMRC may impose penalties for late submissions, incorrect P11D reporting, or underpayment of Class 1A National Insurance contributions. Interest may also be charged on outstanding amounts.

- Administrative corrections: Errors often require revised filings, additional calculations, and communication with affected employees, increasing administrative workload.

- Incorrect employee tax: Employees may pay too little or too much tax, depending on the error. Under-reporting can result in unexpected tax bills, while over-reporting may require refund claims.

- Compliance risks: Repeated inaccuracies can increase scrutiny from HMRC and raise the risk of audits.

Accurate reporting is essential to avoid penalties, ensure correct tax deductions, and maintain compliance.

How Do Benefits in Kind Affect Business Costs and Payroll?

Benefits in kind increase employment costs beyond the value of the perk itself. Employers must also pay Class 1A National Insurance contributions on most benefits, adding to overall expenses.

They also add complexity to payroll. Employers need to calculate benefit values, apply the correct tax treatment, and report them accurately through payroll or P11D. This requires consistent record-keeping and reliable payroll processes.

Benefits in kind, therefore, affect both cost management and payroll accuracy, making structured handling essential for compliance.

How Do Payrolled Benefits in Kind Support Employees and Employers?

Payrolling benefits in kind allows tax on non-cash perks to be collected in real time through payroll. This removes the need for year-end adjustments and simplifies the management of benefits for both employees and employers.

1. Benefits in Kind for Employees

Employees pay tax on benefits gradually through their monthly payroll, avoiding unexpected tax bills. The value of benefits and tax deductions are shown clearly on payslips, improving visibility and making it easier to understand total earnings.

2. Benefits in Kind for Employers

Employers benefit from reduced administrative work, as most P11D reporting is no longer required. Tax is handled through payroll, improving accuracy and reducing year-end processing. This approach also supports better payroll management by aligning tax deductions with regular payroll cycles.

Payrolling benefits, therefore, creates a more efficient, transparent, and consistent approach to managing benefits in kind for both employees and employers.

How Can Direct Payroll Services Improve Your Payroll Management?

Managing payroll alongside benefits in kind requires accurate calculations, compliant reporting, and consistent record management. Direct Payroll Services supports businesses by ensuring payroll processes remain aligned with UK regulations while reducing administrative workload.

Their services help businesses:

- Process employee wages accurately, including benefit-in-kind tax calculations

- Manage PAYE, National Insurance, and HMRC reporting requirements

- Handle payrolling of benefits and P11D submissions efficiently

- Maintain compliant payroll records and reporting systems

- Support pension auto-enrolment and statutory payments

- Reduce manual workload across HR and finance teams

Businesses benefit from structured payroll systems that ensure consistency across each pay cycle and minimise the risk of errors or compliance issues.

Looking to improve payroll accuracy and compliance? Contact Direct Payroll Services today to streamline your payroll processes and confidently manage benefits in kind.

Conclusion

Benefits in kind tax directly affects how non-cash perks are valued, taxed, and reported within payroll. For employees, it affects taxable income and take-home pay, while for employers, it adds compliance responsibilities and costs.

Accurate calculation, correct reporting, and structured payroll processes are essential to avoid errors and penalties. With the shift towards mandatory payrolling of benefits, businesses must ensure their systems and processes are aligned with HMRC requirements.

Frequently Asked Questions

Are There Any Reductions or Allowances Available for Benefit-in-Kind Tax?

Yes. Reductions apply for low-emission or electric vehicles, employee contributions, and limited private use. Some benefits, such as workplace parking and employer pension contributions, are fully exempt from income tax.

What Happens If Benefit-in-Kind Tax Is Not Properly Reported?

Incorrect reporting can lead to HMRC penalties, interest charges, and compliance issues for employers. Employees may also face underpaid tax bills or need to claim refunds, creating additional administrative and financial complications.

How do employers report benefit-in-kind tax to HMRC?

Employers report benefits in kind to HMRC either by submitting P11D and P11D(b) forms at year-end or by payrolling benefits, where tax is collected in real time through payroll.

What does a benefit-in-kind tax mean for employees in the UK?

It means employees pay income tax on the value of non-cash benefits they receive. This value is added to their taxable income, which can reduce take-home pay depending on their tax band.

How is the benefit-in-kind tax calculated on a company car?

It is calculated by applying a percentage (based on CO₂ emissions and fuel type) to the car’s list price. The result is the taxable value, which is then taxed at the employee’s income tax rate.

Where can I find an online calculator for benefit-in-kind tax on vehicles?

You can find an online calculator on the official HMRC website (GOV.UK), which helps estimate benefit-in-kind tax on vehicles using details like list price, CO₂ emissions, and fuel type.