Key Highlights

- Payroll year-end requires accurate record checks, submissions to HMRC, and employee documentation within strict deadlines.

- Employers must verify tax codes, NI categories, benefits, and statutory payments before final payroll runs.

- Final submissions, such as FPS and EPS, confirm year totals and close reporting obligations.

- Employees must receive P60 forms summarising annual earnings and deductions.

- Missing deadlines can trigger penalties, corrections, and administrative delays.

- Errors can still be fixed after submission, but corrections take time and must follow HMRC rules.

- Early preparation reduces compliance risk, workload pressure, and last-minute mistakes.

- Outsourcing payroll year-end helps businesses ensure accuracy, compliance, and peace of mind.

Payroll year-end can feel overwhelming, especially when deadlines, compliance checks, and reporting obligations all converge. If you manage payroll, you know this is not just another processing run. Accuracy is critical, and errors can have lasting consequences.

The UK payroll year ends on 5 April, but compliance does not stop there. Your final RTI submission must align with HMRC records, not just your payroll software totals. You must submit the final Full Payment submission, confirm year-end declarations, reconcile PAYE, update employee data, and issue P60s by 31 May. From 6 April, new tax codes and thresholds apply.

Even small discrepancies in tax, National Insurance, or statutory payments can trigger HMRC queries or penalties.

This guide provides a clear payroll year-end checklist in the correct order. Here’s the order to do things in so you can meet deadlines, stay compliant, and close the tax year with confidence and control.

What Is A Payroll Year-End Checklist?

In the UK payroll, “year-end” refers to the close of the tax year on 5 April. At this point, employers must finalise all payroll records for the period 6 April to 5 April and ensure that cumulative pay, tax, and National Insurance figures match what HMRC expects.

A payroll year-end checklist is a structured sequence of tasks designed to ensure the proper management of this process. It covers reconciling totals, submitting the final Full Payment Submission under Real-Time Information, confirming year-end declarations, and preparing employee documents such as P60S.

Without a clear checklist, the process can quickly become reactive. Discrepancies may go unnoticed, submissions can be delayed, and compliance risks increase. A defined, step-by-step approach ensures payroll is closed accurately, reported correctly, and fully aligned with HMRC requirements before the new tax year begins.

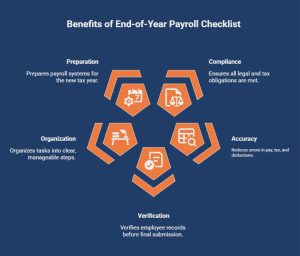

Why Do Employers Need An End Of Year Payroll Checklist?

An end-of-year payroll checklist helps you stay compliant, meet HMRC deadlines, and complete all required payroll tasks without missing critical steps. Year-end involves multiple submissions, record checks, and employee documents, so a clear structure reduces risk and keeps processes accurate.

A checklist helps employers:

- Ensure all filings and reports are submitted on time

- Reduce errors in pay, tax, and deductions

- Verify employee records before final submission

- Organise tasks into clear, manageable steps

- Prepare payroll systems for the new tax year

It also supports a smooth transition into the next payroll cycle by prompting updates to tax codes, thresholds, and settings, so your first pay run of the new year starts correctly.

What Information Should Be Verified Before Payroll Year-End?

Before finalising payroll for the tax year, you need to confirm that all records are accurate, complete, and aligned with HMRC data. This stage acts as your final safeguard against errors, giving you confidence that submissions, calculations, and employee documents will be correct.

1. Employee Details

Start by validating core employee information because this data feeds directly into HMRC reporting and official year-end documents. Check full names, addresses, dates of birth, National Insurance numbers, and employment dates. Even minor inaccuracies can cause submission rejections or mismatched records.

2. Tax Codes

Next, review tax codes to ensure each employee is taxed correctly. Apply any HMRC notifications, confirm coding notices have been implemented, and check that temporary Week 1 or Month 1 indicators are removed unless still required for the new tax year.

3. Benefits And Deductions

Then, examine all benefits and deductions recorded across the year. Confirm pension contributions, salary sacrifice arrangements, student loans, and other deductions match payroll reports. Totals should align with payslips and internal records so final figures remain consistent.

4. Statutory Payments

After that, verify statutory payments such as sick pay, maternity pay, and parental entitlements. Confirm eligibility, payment periods, and recovery amounts. Accurate statutory records protect compliance and ensure employees receive the correct entitlements without adjustments later.

5. Year To Date Totals

Finally, reconcile year-to-date totals for pay, tax, National Insurance, and employer contributions. These cumulative figures must match previous submissions and internal reports. Any mismatch should be investigated and corrected before your final payroll is processed.

Once these checks are complete, your payroll data is fully validated and ready for final processing. This preparation step reduces compliance risk, prevents last-minute corrections, and ensures your year-end submissions are accurate, timely, and stress-free.

What Tasks Must Be Completed Before The Final Payroll Run?

Before processing your final payroll of the tax year, this stage is your last checkpoint to ensure accuracy, compliance, and completeness. Careful review now prevents submission errors, reduces HMRC risks, and ensures employee records reflect the correct financial position for the closing year.

1. Reconcile Year-To-Date Payroll Totals

Cross-check gross pay, PAYE tax, National Insurance, pension deductions, and statutory payments against your year-to-date reports. Ensure figures match previous RTI submissions and internal payroll records. Review tax codes, irregular payments, bonuses, and leavers carefully, as these are common sources of discrepancies.

2. Apply Any Outstanding Corrections

Process any late updates before closing the year. This may include new tax code notices, benefit adjustments, expense corrections, or revised statutory payments. All corrections must be reflected in the final payroll to avoid mismatches with HMRC records.

3. Finalise and Lock The Payroll Period

Confirm all employees are included, deductions are accurate, and no pending entries remain. Once verified, close and lock the payroll period to prevent unintended changes before submission.

4. Generate And Review Final Reports

Produce complete annual payroll reports detailing total pay, deductions, and employer liabilities. Ensure these reports align exactly with RTI figures. Store them securely as compliance evidence and future audit reference.

Completing these steps in sequence ensures your final payroll run is accurate, compliant, and fully prepared for year-end submission.

What Must Be Submitted To HMRC At Year End?

At payroll year-end, employers must complete specific RTI submissions to confirm total pay, deductions, and liabilities for the tax year. These filings formally close your reporting cycle and ensure HMRC records match your payroll before 6 April.

It is important to remember: the pay date determines the tax year, not the period employees worked. If a March payroll is paid on 6 April, it belongs to the new tax year.

1. Submit The Final FPS And Mark It As Final

The Final Full Payment Submission (FPS) confirms each employee’s cumulative earnings, PAYE tax, and National Insurance for the year. It must be submitted on or before the last payday falling on or before 5 April.

You must also mark the submission as the final one for the tax year. This declaration tells HMRC that no further FPS files will follow for that year.

Before submission, verify:

- Employee personal details

- Tax codes and NI categories

- Year-to-date totals

- Statutory payment records

2. Submit An EPS If Adjustments Apply

An Employer Payment Summary (EPS) is required if adjustments affect what you owe HMRC.

Submit an EPS if:

- No employees were paid in the final period

- You forgot to mark the final FPS

- You are reclaiming statutory payments

- You are claiming Employment Allowance

Accurate and timely submissions ensure your payroll year is properly closed and fully compliant.

What Needs To Be Issued To Employees After Year-End?

After completing HMRC reporting, employers must issue the correct statutory documents. This includes providing P60S to all employees employed on 5 April, confirming total annual pay and deductions.

Employees should also receive their final payslip for the tax year. For leavers, a P45 should have been issued at the time of leaving, and year-end is a key point to confirm that those records were processed correctly.

1. P60 Forms

A P60 summarises each employee’s total pay, tax, and National Insurance contributions for the tax year. Employers must issue this document to anyone employed on 5 April.

To ensure accuracy:

- Figures must match submitted payroll data

- Employee details must be correct

- Forms must be issued by 31 May

Providing accurate P60S reduces employee queries and supports their financial recordkeeping.

2. Final Pay Summaries

Final payslips or pay summaries show a detailed breakdown of the last payroll payment. They confirm final earnings, deductions, and statutory payments recorded for the year.

These summaries help employees:

- Review final payment calculations

- Cross-check totals against their P60

- Keep records for loans, tax returns, or audits

Issuing clear year-end documents ensures employees have complete and reliable payroll records.

Confused about the difference between a P45 and a P60? This clear guide breaks down when each form is issued and what employers need to know. Understand how both documents fit into payroll compliance and year-end reporting.

What Errors Should Employers Avoid At Year’s End?

As the final day of the tax year approaches, payroll accuracy becomes critical. Small mistakes during the last pay period can affect compliance, reporting, and employee trust. Careful checks ensure your records meet HMRC requirements and your final RTI submissions are accepted without issue.

1. Incorrect Employee Payroll Records

Incomplete or outdated employee payroll records often cause reporting errors. Always verify names, National Insurance numbers, and pay period data for both current staff and new starters before submitting your final RTI submissions.

2. Unapplied Tax Code Changes

Missing employee tax codes or failing to implement tax code changes can lead to employees paying too much tax or too little. These discrepancies usually surface after submission and require retrospective adjustments to correct.

3. Errors In Final Pay Period Calculations

Mistakes in the final pay period are common, especially when bonuses, deductions, or basic earnings assessment adjustments are added. These must be reviewed carefully so totals match what is reported for the previous tax year.

4. Incorrect Handling Of Leavers And Starters

Failing to process new starters or leavers correctly can distort totals and affect the payment of Class 1 contributions. Always confirm employment dates align with payroll records before the end of the tax year submission.

5. Missing Key Dates And Submission Markers

Missing important dates, such as 5th April or forgetting to submit a final EPS or mark final RTI submissions properly, can trigger compliance alerts. Deadlines are fixed, regardless of whether it is a leap year or a standard tax cycle.

Most payroll errors come from overlooked details rather than complex rules. Checking records, applying updates, and confirming submissions before deadlines protects compliance and prevents corrections later.

How Do You Correct Payroll Mistakes After Submission?

Even well-managed monthly payrolls can contain errors. What matters is how quickly they are corrected. HMRC allows updates after submission, but employers must follow the correct process so records remain compliant and aligned with official reporting standards.

1. Submit Corrected RTI Data

If mistakes are found after filing, you can send updated RTI submissions showing corrected pay, tax, or payment of Class values. This replaces incorrect data previously reported to HMRC.

2. Amend Figures For The Previous Tax Year

If an issue relates to the previous tax year, you must submit revised figures reflecting accurate totals. Corrections should match your internal payroll records and supporting documentation.

3. Adjust Employee Details Or Deductions

Incorrect pay, benefits such as childcare vouchers, or statutory deductions can be updated through revised filings. These corrections ensure HMRC records reflect accurate employee earnings and contributions.

4. Act Before New Reporting Periods Begin

Submitting corrections before the first pay period of the next tax year helps prevent discrepancies from carrying forward. Early action keeps records clean and avoids future reconciliation issues.

Payroll errors after submission are manageable when corrected promptly using the proper method. Timely amendments ensure compliance, maintain accurate reporting, and prevent small mistakes from affecting future payroll cycles.

When Should Employers Start Preparing For Payroll Year-End?

Payroll preparation should never begin at the last minute. Starting early gives employers time to review records, verify data, and confirm calculations before deadlines. Planning also reduces pressure on payroll professionals responsible for final submissions.

1. Start Before The Final Month

Preparation should begin at least two months before the end of the tax year. Early checks allow time to review employee payroll records, confirm national minimum wage compliance, and resolve discrepancies.

2. Review Data Across All Pay Periods

Every pay period across the year should be reconciled. This ensures totals align and highlights any missing or duplicated entries before the final pay period is processed.

3. Confirm Benefits And Deductions

Check benefits such as childcare vouchers, pensions, and statutory payments. These must be accurate before final reporting because they affect totals submitted for the tax year.

4. Prepare For The Start Of The New Tax Year

Preparation should include readiness for the start of the new tax year, including updated tax thresholds, revised employee tax codes, and system updates for the next tax year payroll cycle.

Early preparation gives employers control, accuracy, and confidence. Businesses that review data ahead of deadlines experience fewer surprises and smoother submissions when the final day of the tax year arrives.

Want to reduce payroll costs while staying compliant? Discover how payroll tax exemptions work and whether your business could qualify for valuable savings.

Should You Use Payroll Software Or Outsource Year-End Processing?

As deadlines approach, employers must decide whether to manage payroll internally or rely on payroll services. The right approach depends on your resources, compliance confidence, and how complex your payroll structure is.

1. Managing Year-End With Software

Software can automate calculations, produce reports, and track key dates. For businesses with experienced payroll professionals, this can be efficient, especially when managing straightforward monthly payrolls.

2. Outsourcing To Payroll Professionals

External payroll professionals handle reporting, compliance checks, and submissions. This ensures HMRC requirements are met and reduces internal workload, particularly for businesses without dedicated payroll specialists.

3. Choosing The Right Approach

If your payroll is simple and your team understands RTI submissions, software may be enough. If your payroll involves adjustments, multiple pay types, or tight deadlines, outsourcing often provides greater accuracy and reassurance.

The best payroll approach is the one that guarantees accuracy, meets deadlines, and keeps your business compliant. Whether using software or payroll services, reliability and compliance should guide your decision.

Want to simplify client payroll without increasing workload? Discover how payroll outsourcing for accountants can save time, reduce compliance risk, and help you scale services confidently.

How Can Direct Payroll Services Support Your Payroll Year-End?

Payroll year-end requires precise checks, accurate reporting, and strict adherence to HMRC requirements. When deadlines approach, managing everything internally can place pressure on your team, especially when employee payroll records, tax code changes, and final RTI submissions must all align correctly.

Direct Payroll Services supports employers by handling calculations, validations, and submissions in a structured and compliant way. Experienced payroll professionals review each pay period, reconcile figures for the previous tax year, and ensure all reports are accurate before filing, reducing the risk of errors or penalties.

They also prepare your payroll for the start of the new tax year, making sure systems, thresholds, and records are updated from the first pay run. This allows you to close the year confidently, stay compliant, and focus on running your business rather than worrying about payroll deadlines.

Need help with payroll year-end or ongoing payroll support? Contact our team today and let Direct Payroll Services handle your payroll accurately, securely, and on time.

Final Thoughts

Payroll year-end is manageable when approached with structure, preparation, and accurate reporting. By verifying records, meeting key deadlines, and submitting correct RTI filings, employers can close the tax year confidently and avoid penalties or corrections.

Starting early, reviewing data carefully, and understanding HMRC requirements reduces risk and workload. Whether handled internally or with professional payroll services, a clear year-end checklist ensures compliance, protects employees, and sets your business up for a smooth start to the new tax year.

Frequently Asked Questions

What are the most common payroll year-end mistakes, and how can you avoid them?

Common payroll year-end mistakes include incorrect employee details, missed tax code updates, and late submissions. You can avoid them by reviewing records carefully, reconciling totals before filing, using a checklist, and starting preparation early enough to correct discrepancies without deadline pressure.

How can small businesses streamline the payroll year-end process?

Small businesses can streamline payroll year-end by using reliable payroll software to automate calculations, reports, and submissions. Outsourcing to payroll professionals is another option, reducing administrative workload while ensuring compliance, accuracy, and timely filings with HMRC requirements.

Is there a payroll year-end checklist template for UK employers?

Yes, many payroll providers and official resources offer structured templates for UK employers. These help track submissions, verify employee payroll records, and manage deadlines, ensuring all required tasks are completed accurately before the end of tax year reporting.

How do you reconcile payroll at year’s end?

To reconcile payroll at year’s end, compare year-to-date payroll totals with internal records for pay, tax, and deductions. Confirm each employee’s figures match reports and submissions so P60 data and HMRC records remain consistent and accurate.

What do employers need to do for the payroll year-end?

Employers must complete the final pay run, verify payroll records, submit final RTI filings, confirm National Insurance contributions, and issue P60S by 31 May. They should also prepare payroll systems, tax codes, and thresholds for the next tax year.

Are there any key deadlines I need to be aware of for payroll year-end processing in 2025?

Key payroll deadlines include 5 April for the tax year end, final submissions on or before the last payday, P60 distribution by 31 May, and P11D reporting by 6 July. Missing these dates can trigger penalties or compliance notices.

What items are typically included in a payroll process?

A payroll process includes salaries, overtime, bonuses, statutory payments, tax, National Insurance, pensions, and benefits. All earnings and deductions must be calculated correctly and recorded in payroll reports so submissions reflect accurate employee totals.