Key Highlights

- Limited companies must register as an employer with HMRC before paying directors or employees.

- PAYE registration is required to correctly manage tax deductions, National Insurance, and payroll reporting.

- HMRC-recognized payroll software helps automate RTI submissions, payslips, and payroll calculations.

- Accurate employee onboarding reduces the risk of payroll errors, incorrect tax codes, and reporting issues.

- Employers must manage workplace pension duties, payroll records, and PAYE deadlines throughout the tax year.

- Common payroll mistakes, such as late RTI submissions or incorrect deductions, can result in HMRC penalties.

- Outsourcing payroll can reduce administrative workload and improve payroll compliance for growing businesses.

- Direct Payroll Services supports limited companies with payroll setup, PAYE administration, and ongoing payroll management.

Setting up payroll is one of the first compliance challenges many limited companies encounter after hiring employees or paying directors. Although the process itself is manageable, errors involving PAYE registration, tax deductions, or HMRC submissions can disrupt cash flow, delay reporting, and create avoidable administrative pressure.

Payroll responsibilities extend far beyond issuing salaries. Employers must maintain accurate employee records, submit Real Time Information (RTI) filings, manage workplace pension contributions, and meet strict HMRC deadlines throughout the tax year. Even small mistakes, such as using the wrong tax code or missing a submission date, can result in penalties or payroll disputes.

This guide explains how to set up payroll for a limited company in the UK, covering HMRC employer registration, payroll software selection, employee onboarding requirements, PAYE obligations, and the practical steps businesses can take to avoid common payroll problems from the outset.

What Is Payroll for a Limited Company?

Payroll for a limited company is the process of paying directors and employees while managing PAYE tax deductions, National Insurance contributions, workplace pension payments, and HMRC reporting requirements.

Unlike sole traders, limited companies must operate a Pay As You Earn (PAYE) scheme when paying salaries above HMRC thresholds. This requires employers to calculate deductions accurately, submit Real Time Information (RTI) reports to HMRC, and maintain payroll records throughout the tax year. Even companies with a single director may need payroll if a salary is taken through the business.

What Do You Need Before Setting Up Payroll?

Setting up payroll involves more than paying employee salaries. Limited companies, particularly small companies, must also budget for employer payroll costs, which can increase as the workforce grows. Failing to account for these expenses early can create cash flow pressures and make payroll liabilities harder to manage.

In addition to employee wages, employers may need to cover:

- Employer National Insurance contributions

- Workplace pension contributions

- Payroll software subscriptions

- Payroll outsourcing fees, if applicable

- Statutory payments such as maternity or sick pay

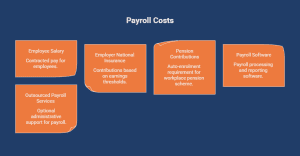

| Payroll Cost | Employer Responsibility |

|---|---|

| Employee Salary | Contracted pay |

| Employer National Insurance | Based on earnings thresholds |

| Pension Contributions for the workplace pension scheme | Auto-enrolment requirement |

| Payroll Software | Payroll processing and reporting |

| Outsourced Payroll Services | Optional administrative support |

Understanding these costs before the first payroll run helps businesses budget accurately and avoid unexpected expenses as payroll obligations increase.

How to Set Up Payroll For Limited Company?

Setting up payroll involves more than registering for PAYE and issuing salaries. Employers must establish a system that calculates deductions accurately, reports payroll information to HMRC on time, and keeps employee records organised from the first pay cycle onward to comply with HMRC regulations. Problems during setup often create ongoing reporting and compliance issues that become harder to correct later.

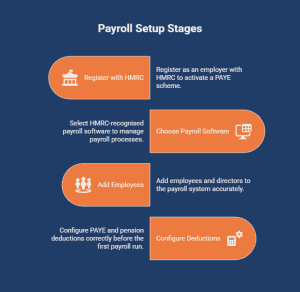

For most limited companies, payroll setup follows four core stages: registering with HMRC, selecting payroll software, adding employees and directors, and configuring PAYE and pension deductions correctly.

1. Register as an Employer With HMRC

Before paying employees or directors, limited companies must register as an employer with HMRC to activate a PAYE scheme. Without registration, businesses cannot submit payroll information or process tax deductions legally, which may lead to any tax due remaining unpaid.

Accounts Office Reference number

| HMRC Reference | Purpose |

|---|---|

| PAYE Reference | Used for payroll submissions and employee reporting |

| Accounts Office Reference | Used when paying PAYE liabilities to HMRC |

Late registration is a common payroll mistake for newly formed companies. Businesses that wait until payroll deadlines approach often encounter delays accessing PAYE references, which can postpone salary processing and RTI submissions.

Once registration is complete, employers can begin configuring payroll systems and employee records.

2. Choose HMRC-Recognised Payroll Software

Payroll software becomes the operational centre of the payroll process. It calculates deductions, generates payslips, manages outstanding balance and submits Real Time Information (RTI) reports, helping businesses maintain accurate payroll records throughout the tax year.

When comparing payroll software, businesses should evaluate:

- RTI submission functionality

- Pension integration

- Payslip generation

- Employee record management

- Scalability for future growth

- Compatibility with accounting software

Smaller businesses sometimes rely on manual spreadsheets during early payroll setup. However, manual payroll processes significantly increase the risk of incorrect tax calculations, missed pension deductions, and reporting errors, particularly once additional employees are added.

| Payroll Method | Operational Risk |

|---|---|

| Manual Payroll | Higher risk of calculation and reporting errors |

| Payroll Software | Automated calculations and reporting support |

Choosing software that aligns with business size and payroll complexity helps reduce administrative pressure as the company grows.

3. Add Employees and Directors to Payroll

Once payroll software is configured, employers can begin adding employees and directors to the system. Accurate onboarding is essential because payroll errors often begin with incomplete employee setup or incorrect tax information.

Businesses typically need to record:

- Directors must also be included in payroll, along with their payroll ID, if they receive salaries through the company. This applies even where the director is the only employee on the payroll system.

- National Insurance numbers

- Tax codes

- Employment start dates

- Salary information

- Pension eligibility status

Directors must also be included in payroll if they receive salaries through the company. This applies even where the director is the only employee on the payroll system.

Incorrect employee setup can create problems immediately. For example, using the wrong tax code during onboarding may result in underpaid tax, employee complaints, and later corrections through HMRC.

4. Configure PAYE and Pension Deductions

Once employees are added, employers must configure payroll deductions correctly, including charity donations, before the first payroll run. Incorrect deduction settings are one of the most common causes of payroll adjustments and reporting discrepancies.

Payroll systems typically calculate:

- Income Tax deductions

- Employee National Insurance contributions

- Employer National Insurance contributions

- Workplace pension contributions

- Student loan repayments were applicable

Auto-enrolment pension duties also apply to eligible employees. Employers are responsible for assessing worker eligibility, enrolling qualifying staff, and maintaining accurate contribution records throughout employment.

Accurate deduction configuration is critical because payroll mistakes rarely remain isolated. Incorrect deductions can affect payslips, pension reporting, HMRC liabilities, and employee confidence simultaneously.

What Payroll Compliance Rules Should Limited Companies Follow?

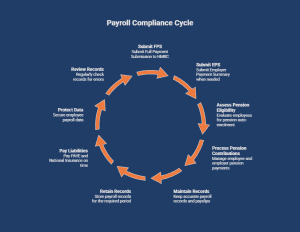

Once payroll is set up, employers must meet several ongoing compliance requirements to avoid penalties, reporting issues, and payroll disputes. Keeping track of these obligations helps ensure payroll, including gross pay, remains accurate and compliant throughout the tax year.

Payroll Compliance Checklist

- Submit a Full Payment Submission (FPS) to HMRC on or before each payday

- Submit an Employer Payment Summary (EPS) when adjustments or recovery claims apply

- Assess eligible employees for workplace pension auto-enrolment

- Process employee and employer pension contributions correctly

- Maintain accurate payroll records, payslips, and employee payment information

- Retain payroll records for the required HMRC retention period

- Pay PAYE and National Insurance liabilities by the relevant deadlines

- Protect employee payroll data in accordance with UK data protection requirements

- Review payroll records regularly to identify reporting, deduction, or payment errors

Following these requirements helps employers avoid reporting errors, missed deadlines, and payroll compliance issues throughout the tax year.

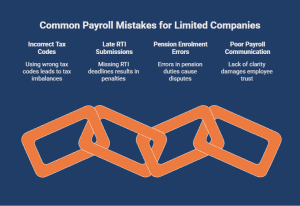

What Are the Most Common Payroll Mistakes Limited Companies Make?

Most payroll mistakes are not caused by software failures. They usually happen because businesses rush payroll setup, overlook reporting deadlines, or rely on incomplete employee information. Small payroll errors can quickly escalate into tax corrections, employee disputes, pension issues, or HMRC penalties if they continue across multiple pay periods.

Newly formed limited companies are particularly exposed because payroll responsibilities often expand faster than expected once employees, pensions, and RTI reporting become ongoing obligations.

1. Incorrect Tax Codes

Using the wrong tax code can result in employees paying too much or too little tax, including not paying the correct amount of tax, creating payroll corrections that often take months to resolve. This problem commonly appears during employee onboarding when businesses rely on outdated information or apply emergency tax codes incorrectly.

Payroll issues typically arise when:

- A new employee joins without a valid P45

- Starter checklist information is incomplete

- HMRC tax code updates are missed

- Temporary tax codes remain active for too long

Incorrect tax deductions rarely affect payroll in isolation. Employees may question payslips, request repayment explanations, or face unexpected tax adjustments later in the year. Regular payroll reviews help identify coding issues before they create larger reporting problems.

2. Late RTI Submissions

HMRC requires employers to submit payroll information on or before each payday through Real Time Information (RTI) reporting. Late Full Payment Submissions (FPS) are one of the most common compliance failures for small businesses managing payroll internally using their online account.

Late submissions often happen because:

- Payroll is processed too close to payday

- Employee records are incomplete

- Payroll approvals are delayed

- Businesses rely on manual payroll tracking

| Payroll Issue | Potential Consequence |

|---|---|

| Late FPS Submission | HMRC penalties and warning notices |

| Incorrect RTI Data | Payroll corrections and reporting discrepancies |

| Missed PAYE Payment | Interest charges and outstanding liabilities |

Businesses that leave payroll processing until the last minute usually increase the risk of filing errors and rejected submissions.

3. Pension Enrolment Errors

Auto-enrolment pension duties create additional compliance pressure for employers, particularly during employee onboarding or salary changes. Missing pension assessments or calculating contributions incorrectly can trigger disputes with employees and intervention from The Pensions Regulator.

Common pension mistakes include:

- Failing to assess employee eligibility correctly

- Missing enrolment deadlines

- Applying incorrect contribution percentages

- Forgetting to update pension deductions after salary changes

Payroll software can automate much of the assessment process, but employers still remain responsible for ensuring contributions and enrolment records stay accurate throughout employment.

4. Poor Payroll Communication

Payroll problems become more difficult to manage when employees do not understand how their pay or deductions are calculated under the necessary data protection rules. Poor communication often increases payroll queries, delays issue resolution, and damages employee confidence unnecessarily.

Communication issues usually involve:

- Unclear payslips

- Unexplained deduction changes

- Delayed responses to payroll queries

- Missing communication around payroll dates or pension contributions

For example, an employee who notices an unexpected tax deduction without explanation may assume they have been underpaid, even when the calculation itself is correct. Clear payroll communication helps prevent avoidable disputes and reduces administrative workload for employers handling payroll internally.

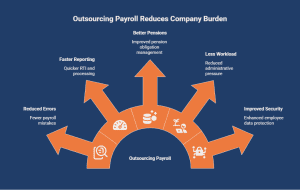

Should Limited Companies Outsource Payroll?

Many small limited companies in the United Kingdom initially manage payroll internally, but payroll responsibilities become more demanding as employee numbers, pension obligations, and reporting requirements increase, especially regarding the eligibility criteria for auto enrolment. Businesses that struggle with payroll deadlines or recurring errors often find outsourcing more efficient and lower risk.

Outsourcing payroll also reduces the administrative pressure associated with PAYE reporting, pension management, and payroll compliance.

Benefits of Outsourced Payroll

Professional payroll providers help businesses reduce errors, improve reporting accuracy, and stay compliant with changing HMRC requirements.

Key benefits include:

- Reduced risk of payroll errors and penalties

- Faster RTI reporting and payroll processing

- Better management of pension obligations

- Less administrative workload for internal teams

- Improved security for employee payroll data

For growing businesses, outsourcing often becomes more cost-effective than managing payroll corrections, compliance issues, and internal administration separately.

When Outsourcing Becomes Necessary

Payroll outsourcing becomes increasingly valuable when businesses:

- Hire more employees

- Manage variable pay structures

- Expand payroll responsibilities

- Struggle with reporting deadlines

- Experience repeated payroll errors

For some companies, payroll complexity grows gradually. For others, especially businesses scaling quickly, payroll administration can become difficult to manage internally within a short period of time.

How Can Direct Payroll Services Help Limited Companies?

Setting up payroll internally can quickly become time-consuming once PAYE reporting, pension duties, employee onboarding, and HMRC deadlines begin overlapping. Many limited companies struggle with payroll administration not because the process is impossible, but because compliance mistakes, especially when they need to pay PAYE bills, become costly when payroll is handled inconsistently.

Direct Payroll Services supports limited companies with payroll setup, PAYE registration, RTI submissions, pension administration, and ongoing payroll management. Their services are designed to help businesses reduce reporting errors, improve payroll accuracy, and maintain compliance as payroll responsibilities grow.

Support typically includes:

- HMRC employer registration

- Payroll software setup

- Employee and director payroll onboarding

- PAYE and pension administration

- RTI reporting support

- Ongoing payroll processing and compliance management

For growing businesses, outsourcing payroll can reduce administrative workload significantly while improving confidence that payroll obligations are being managed correctly. Businesses looking to simplify payroll setup or reduce compliance risk can contact Direct Payroll Services.

Conclusion

Setting up payroll for a limited company requires more than simply paying salaries on time, especially for international businesses doing this for the first time. Employers must manage PAYE registration, tax deductions, including Construction Industry Scheme compliance, RTI submissions, pension obligations, and payroll recordkeeping accurately to remain compliant throughout the tax year. Small setup mistakes can quickly create reporting issues, employee disputes, and avoidable HMRC penalties if they are not identified early.

A structured payroll process helps businesses reduce administrative pressure, improve reporting accuracy, and maintain employee confidence as operations grow. Whether managing payroll internally or using external support, maintaining organised payroll systems and ensuring proper financial management while meeting reporting deadlines consistently is essential for long-term compliance and financial stability.

Frequently Asked Questions

Do I need to set up payroll if I am the only director and employee?

Yes, if your salary exceeds HMRC thresholds or you receive taxable benefits, you must set up payroll and register for PAYE, even if you are the only director and employee of the company.

How do I submit payroll information to HMRC?

Employers submit payroll information to HMRC through payroll software using Real Time Information (RTI) reports, including a Full Payment Submission (FPS) sent on or before each employee’s payday.

What are the ongoing payroll deadlines for limited companies?

Limited companies must submit a Full Payment Submission (FPS) on or before each payday and pay PAYE liabilities for benefits such as a company car to HMRC by the 22nd of the following tax month when paying electronically.

Are there any common mistakes to avoid when setting up payroll for a limited company?

Yes, common payroll mistakes include late PAYE registration, incorrect tax codes, missed RTI submissions, pension enrolment errors, and incomplete employee records, all of which can lead to HMRC financial penalties and payroll corrections.

Can I run payroll myself as a limited company director?

Yes, directors can manage payroll themselves using HMRC-recognised payroll software. However, they remain responsible for PAYE calculations, RTI reporting, pension duties, and meeting payroll deadlines.

How long does it take to register for PAYE with HMRC?

PAYE registration typically takes several working days. Businesses should register before their first payday to ensure they receive their PAYE and Accounts Office references in time.

Can I pay directors through dividends instead of payroll?

Directors can receive dividends, but salaries must still be processed through payroll when PAYE rules apply. Dividends do not replace payroll reporting obligations or PAYE requirements.