Key Highlights

- Contractor pay depends on worker classification, IR35 status, and contractor location

- Businesses can handle contractor payments through invoices, payroll, or umbrella companies

- IR35 determines whether contractor payments require tax withholding via payroll

- Paying international contractors involves currency, tax compliance, and local labour laws

- Contractor pay rates are higher due to the lack of benefits and employment rights

- Misclassification and poor processes can lead to penalties, back taxes, and payment risks

Paying contractors in the United Kingdom is no longer a simple transaction. What looks straightforward on the surface often involves multiple layers of tax rules, worker classification, and reporting requirements.

The shift towards remote work and access to a global talent pool has added another dimension. Businesses are now handling international contractor payments, managing currency conversion, and working across different countries with their own labour laws and payment standards.

On top of this, IR35 has changed how contractor payments are assessed. The distinction between contractor and employee is not always clear, and that decision directly affects how payments are taxed and processed.

This guide explains how to pay contractors correctly, structure payments efficiently, and handle everything in line with HMRC expectations.

What Is Contractor Pay and Why Does It Work Differently From Salaries?

Contractor pay refers to payments made to independent professionals for services defined within a scope of work, without forming an employment relationship. Unlike salaries, contractor payments are not automatically processed through PAYE and do not include built-in tax deductions or statutory contributions.

The key difference lies in how tax is handled.

In most cases, contractors are responsible for managing their own tax, including income tax and National Insurance. They receive full payments and report earnings through self-assessment. However, when IR35 applies, businesses must treat contractor payments as employment income and apply PAYE, including tax withholding and National Insurance contributions.

This means the same role can be taxed in two completely different ways depending on classification. That is why getting the structure right at the start is critical. While this model gives businesses flexibility in how they engage talent, it also places greater responsibility on accurate classification, correct tax treatment, and proper reporting to HMRC.

How Does Contractor Pay Compare to Employee Salary?

The differences between contractors and employees directly affect how payments are structured, taxed, and reported. Understanding this distinction helps you choose the right payment approach before processing any payments.

| Factor | Contractor | Employee |

|---|---|---|

| Tax handling | Self-managed or PAYE if IR35 applies | PAYE deducted |

| Employment rights | Limited | Full statutory rights |

| Payment structure | Flexible, project-based | Fixed salary |

| National Insurance | Self-managed or deducted under IR35 | Employer and employee contributions |

| Pension & statutory benefits | Not included in contractor pay | Includes pension, sick pay, and holiday pay |

What Determines How You Should Pay Contractors?

Once the fundamentals are clear, the next step is deciding how to structure contractor payments correctly. This is not a fixed process. It depends on classification, tax treatment, and where the contractor is based.

Getting these inputs right at the start shapes how payments are processed, taxed, and reported.

1. Worker Classification

Worker classification is the foundation of contractor payments. If a contractor is incorrectly classified, it can lead to worker misclassification, back taxes, and potential penalties.

This decision determines whether payments are treated as independent contractor payments or as employment income.

To assess classification accurately, businesses must look beyond job titles and focus on how the work is actually performed.

Key Factors That Influence Classification

- Right of substitution

Can the contractor send someone else to complete the work? A genuine right of substitution supports contractor status. - Control and supervision

Does the business control how, when, and where the work is done? Higher control points towards employment. - Mutuality of obligation

Is the business obligated to provide work, and is the contractor expected to accept it? Ongoing obligation suggests an employment relationship.

These factors are central to determining whether a contractor should be treated as self-employed or as a deemed employee.

2. IR35 and Compliance

IR35 determines whether a contractor should be treated as an employee for tax purposes. If applicable, paying contractors through payroll becomes mandatory. This means applying PAYE, handling tax withholding, and meeting reporting obligations as part of the payment process.

The outcome of your classification assessment directly feeds into this decision.

3. Contractor Location

Location introduces additional requirements. Paying foreign independent contractors involves understanding local labour laws, managing international transfers, and ensuring compliance across different countries.

This becomes more relevant when handling international contractor payments, where currency, tax rules, and reporting standards vary across jurisdictions.

Getting these factors right upfront ensures you choose the correct payment structure from the start. It sets the foundation for accurate tax treatment, smoother processing, and consistent HMRC reporting.

What Are the Main Payment Options for Contractor Payments in the UK?

After defining classification and compliance requirements, the next step is choosing how contractor payments will be made. This is not a one-size-fits-all decision. Each method differs in how tax is handled, how payments are processed, and how much responsibility sits with the business.

In the United Kingdom, contractor payments are typically managed through four main approaches.

1. Paying Contractors via Invoices

This method is commonly used when contractors operate outside IR35. Contractors submit invoices based on agreed payment terms, and businesses process payments through bank transfers or direct deposit into the contractor’s bank account.

It offers flexibility and low administrative effort, but relies on correct classification and the contractor managing their own tax obligations.

2. Paying Contractors Through Limited Companies (PSC)

Many UK contractors operate through Personal Service Companies (PSCs). In this structure, the business contracts with the contractor’s limited company rather than the individual. Payments are made to the company’s bank account against invoices. The contractor then manages their own salary, dividends, and taxes through their company.

However, IR35 still applies. If the engagement falls inside IR35, the business must deduct tax before making payments, even when paying a limited company.

3. Paying Contractors Through Payroll

When IR35 applies, paying contractors through payroll becomes necessary. This involves applying PAYE, HMRC, handling tax withholding, and making National Insurance contributions.

This structure is often referred to as contractor PAYE umbrella IR35, where tax and reporting responsibilities sit with the business or an intermediary.

4. Using Umbrella Companies

Umbrella companies act as an intermediary employer. They handle payment processing, tax deductions, and reporting, reducing the administrative burden on businesses.

This approach is useful when managing multiple contractors or when IR35 applies across engagements.

How Do These Contractor Payment Methods Compare?

Each method comes with trade-offs in terms of cost, control, and administrative effort. The right choice depends on how your contractors are engaged and how much responsibility you want to manage internally.

| Method | Tax Handling | Payment Processing | Compliance Risk | Cost | Admin Burden | IR35 Suitability |

|---|---|---|---|---|---|---|

| Invoice (Sole trader) | Contractor | Bank transfers | Medium | Low | Low | Outside IR35 |

| Limited Company (PSC) | Contractor or employer (IR35 dependent) | Bank transfers | Medium | Medium | Medium | Inside & Outside IR35 |

| Payroll (PAYE) | Employer | Direct deposit | Low | Medium to High | Medium | Inside IR35 |

| Umbrella | Third-party | Managed system | Low | High | Low | Inside IR35 |

Invoice and PSC models offer more flexibility when engagements fall outside IR35, while payroll and umbrella structures provide greater control and consistency when IR35 applies.

The right payment method depends on how your contractors are classified and how IR35 applies to each engagement. Getting this decision right early simplifies tax handling, reporting, and ongoing contractor relationships.

How Does IR35 Impact Contractor Payments?

Once payment methods are defined, IR35 becomes the deciding factor in how contractor payments are actually processed. It determines whether payments should be treated as independent contractor income or as employment income for tax purposes.

Understanding IR35 upfront ensures that contractor payments are structured correctly and remain compliant with HMRC requirements.

Who Decides IR35 Status?

In the United Kingdom, the responsibility for determining IR35 status depends on the organisation hiring the contractor.

- Medium and large businesses are responsible for assessing IR35 status

- Small businesses can pass this responsibility to the contractor

The decision must reflect actual working arrangements, not just contract terms.

What Is a Status Determination Statement (SDS)?

When a business is responsible for IR35, it must issue a Status Determination Statement (SDS).

An SDS:

- Confirms whether the engagement is inside or outside IR35

- Explains the reasoning behind the decision

- Must be shared with the contractor and any agency involved

Without a valid SDS, the business remains responsible for tax and compliance.

What Happens When a Contractor Is Inside IR35?

When a contractor falls inside IR35, payments must be processed through payroll. This includes tax withholding, National Insurance contributions, and reporting through PAYE.

This increases responsibility for the business and reduces the contractor’s take-home pay due to deductions at source.

What Happens When a Contractor Is Outside IR35?

When a contractor is outside IR35, payments are made in full against invoices. Contractors manage their own tax through self-assessment or company structures.

This approach offers more flexibility but depends on accurate classification.

Why Do IR35 Mistakes Matter?

Incorrect classification can lead to back taxes, penalties, and HMRC investigations. It can also disrupt operations if issues are identified later. Getting IR35 right at the start protects financial outcomes and maintains stable contractor relationships.

In practice, IR35 is not just a tax rule. It directly determines how contractor payments are structured, processed, and reported.

Still unsure how IR35 actually changes the way contractors are paid? This guide breaks down the key differences between IR35 and PAYE, so you can understand when payroll applies, how tax is handled, and what it means for your business.

How Are Contractor Payments Taxed in Different Scenarios?

Once classification and payment method are clear, the next step is understanding how contractor payments are taxed. This depends on structure, not just the role.

1. Outside IR35

Payments are made in full without tax withholding.

- Contractors handle income tax via self-assessment

- National Insurance is paid directly

- PSC contractors may split income between salary and dividends

This offers flexibility but places full tax responsibility on the contractor.

2. Inside IR35

Payments are treated as employment income.

- PAYE is applied before payment

- Income tax and National Insurance are deducted

- The business or fee-payer reports to HMRC

This reduces compliance risk but lowers take-home pay.

3. Limited Company (PSC)

Payments are made to the contractor’s company.

- Income is taken as salary, dividends, or both

- Corporation tax applies to company profits

If IR35 applies, tax must be deducted before payment, even when paying a company.

4. International Contractors

Tax treatment depends on jurisdiction and tax treaties.

- UK businesses usually do not withhold tax

- Contractors pay tax in their home country

- Double taxation agreements determine tax liability

Currency conversion and local tax rules also affect final payouts.

Why Payment Structure Matters?

The payment structure directly affects tax, reporting, and overall cost.

- Invoice model: contractor manages tax

- Payroll model: tax deducted at source

- Umbrella/EOR: third party handles compliance

Choosing the right structure ensures accurate tax treatment and avoids downstream issues.

How Do You Handle Paying International Contractors?

As businesses expand beyond the United Kingdom, contractor payments involve more than just transferring funds. You are dealing with cross-border tax rules, local labour laws, and different payment systems.

A structured approach helps ensure consistency, accurate reporting, and smooth international transactions.

What Should You Consider When Paying Foreign Independent Contractors?

When paying foreign independent contractors, businesses must align with legal requirements in the contractor’s home country. This includes correct tax forms, a clear scope of work, and proper worker classification.

Getting this wrong can lead to penalties, back taxes, or compliance issues across jurisdictions.

What Are the Best Payment Methods for International Contractor Payments?

Common payment options include:

- International wire transfers

- Digital and online payment platforms

- Global payroll systems

Each option differs in transaction fees, processing time, and visibility into payment status.

How Do Currency and Cross-Border Payments Affect Processing?

Payments across different currencies involve exchange rate fluctuations and conversion costs. International transfers may also include intermediary fees and delays.

Clear payment terms and a defined payment schedule help maintain consistency.

What Is Permanent Establishment Risk?

Permanent Establishment (PE) risk arises when contractor activity creates a taxable presence in a foreign country.

This can trigger local tax obligations, registration requirements, and additional reporting.

How Do Tax Treaties Affect International Contractor Payments?

Tax treaties prevent double taxation by defining where income is taxed and how tax is applied.

Understanding these agreements helps reduce unnecessary tax exposure and ensures correct withholding.

When Should You Use an Employer of Record (EOR)?

An Employer of Record (EOR) allows businesses to hire in a foreign country without setting up a local entity.

It manages payroll, tax compliance, and local labour laws, while reducing PE risk.

What Are Common Mistakes in International Contractor Payments?

- Ignoring local labour laws

- Incorrect tax handling or missing documentation

- Delayed payments

- Poorly defined scope of work

- Overlooking PE risk or tax treaties

Managing international contractor payments requires coordination across tax, legal, and financial processes. A structured setup ensures payments remain consistent, compliant, and scalable.

Payroll mistakes often come from assumptions rather than rules. From IR35 confusion to tax handling errors, small misunderstandings can lead to bigger issues over time. Explore the most common myths and what actually applies in practice.

How Are Contractor Pay Rates Structured?

Once payment methods and compliance factors are clear, the next consideration is cost. Contractor pay rates are typically higher than employee salaries, but they reflect a different structure of risk and responsibility.

Understanding how these rates are built helps businesses plan budgets and make informed hiring decisions.

What Influences Contractor Pay Rate?

Several factors determine contractor pay rate, including:

- Skill level and experience

- Market demand

- Scope of work

- Project duration

Specialised roles or short-term projects often command higher rates due to urgency and expertise.

How Does Contractor Cost Compare to Employee Cost?

The cost difference between contractors and employees goes beyond base pay. It includes benefits, long-term commitments, and operational flexibility.

This comparison highlights the broader cost structure.

| Cost Element | Contractor | Employee |

|---|---|---|

| Base cost | Higher | Lower |

| Benefits | Not included | Included |

| Flexibility | High | Limited |

While contractor pay rates may appear higher, the overall cost structure can be more flexible depending on business needs.

Do Contractors Receive Sick Pay or Employment Benefits?

Contractor payments are structured differently from employee salaries, especially when it comes to benefits and entitlements.

This distinction is important for setting expectations and avoiding misunderstandings.

Why Contractor Sick Pay Is Not Standard?

Contractors are not classified as employees, which means contractor sick pay is not a statutory requirement. Their payments are designed to cover the full value of their work without additional benefits.

They are responsible for managing their own financial protection, including time off.

When Exceptions May Apply?

In some cases, umbrella companies or employer of record arrangements may include limited benefits within the payment structure.

However, these are exceptions and not standard across most contractor relationships.

Understanding this difference helps businesses structure payments clearly and avoid confusion around entitlements.

What Are the Biggest Risks in Contractor Payments?

Even with the right structure in place, contractor payments can create issues if not managed carefully. Most problems arise from incorrect classification, tax handling, or gaps in execution.

Identifying these early helps avoid financial exposure and operational disruption.

1. Worker Misclassification

Incorrect classification is one of the most common issues. When contractors are treated as self-employed but operate like employees, it creates disguised employment risk, particularly under IR35.

This can lead to back taxes, penalties, and reclassification of past payments.

2. HMRC Retrospective Investigations

HMRC can review contractor arrangements years after payments have been made. If inconsistencies are found, businesses may face retrospective tax liabilities, interest, and penalties.

These investigations often focus on IR35 decisions and classification accuracy.

3. Tax and Reporting Errors

Errors in tax handling, missing documentation, or incorrect filings can trigger compliance issues. Inconsistent reporting increases the likelihood of scrutiny and financial penalties.

4. VAT Errors

For VAT-registered contractors, invoices may include VAT that must be handled correctly.

Common issues include:

- Incorrect VAT treatment

- Failure to reclaim VAT where applicable

- Misreporting VAT in contractor payments

5. Payment Delays and Errors

Late or inconsistent payments can affect contractor relationships and impact access to skilled professionals. Clear payment terms and a defined payment schedule help maintain consistency and trust.

Managing contractor payments effectively requires clear processes, accurate classification, and ongoing oversight. Getting these fundamentals right reduces exposure and keeps operations stable.

When Should You Use Payroll or Global Payroll Support?

As contractor payments scale across teams and locations, managing them internally becomes more demanding. This is where structured payroll support becomes valuable.

Outsourcing simplifies processes while improving accuracy, consistency, and compliance across all contractor payment activities.

What Are the Signs You Need Payroll Support?

As contractor operations grow, certain challenges begin to surface. These are early indicators that internal systems may no longer be sufficient.

If these issues are recurring, it is a clear sign that structured payroll support is needed.

- Managing multiple contractors across different countries

- Handling international contractor payments regularly

- Struggling with tax compliance and reporting requirements

What Payroll Solutions Offer?

Payroll and global payroll services are designed to standardise and simplify contractor payment management at scale.

They centralise processes, reduce manual effort, and ensure consistency across different regions and compliance frameworks.

- Payment processing

- Tax compliance and reporting

- Worker classification management

- International transactions

They also reduce administrative workload and minimise compliance risk.

At scale, using payroll support shifts contractor payment management from reactive problem-solving to a controlled, reliable process.

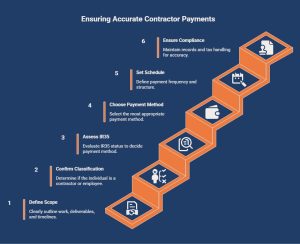

How to Pay Contractors Step by Step?

Paying contractors correctly requires more than just processing payments. Each step, from defining the work to ensuring compliance, directly impacts how payments are structured, taxed, and managed. Following a clear process helps reduce errors, avoid penalties, and maintain consistency.

How Do You Define the Scope of Work and Payment Terms?

Start by clearly outlining the scope of work, deliverables, timelines, and agreed payment terms. This sets expectations early and ensures both parties are aligned before any payment process begins.

How Do You Confirm Worker Classification?

Determine whether the individual is a contractor or should be treated as an employee. Proper classification is critical to avoid worker misclassification, back taxes, and compliance issues.

How Do You Assess IR35 Status?

Evaluate whether the contractor falls inside or outside IR35. This decision determines whether payments should be processed through payroll or handled via invoices.

How Do You Choose the Right Payment Method?

Select the most appropriate payment method based on classification and IR35 status. Options may include invoices, payroll, or umbrella arrangements.

How Do You Set Up a Payment Schedule and Structure?

Define how and when payments will be made. A clear payment schedule ensures timely payments and helps maintain strong contractor relationships.

How Do You Ensure Tax Compliance and Documentation?

Maintain accurate records, apply correct tax handling, and ensure all documentation is in place. This reduces the risk of penalties and supports smooth reporting.

Getting these steps right ensures contractor payments are accurate, compliant, and easy to manage.

A structured approach reduces risk while improving efficiency across your payment process.

How Can Direct Payroll Services Simplify Contractor Payments?

As contractor payments grow in volume and complexity, managing IR35, classification, and compliance internally becomes harder to control. Small errors can lead to penalties, delays, and operational friction.

Direct Payroll Services helps streamline contractor payments across the United Kingdom by handling payroll processing, IR35 compliance, tax reporting, and international contractor payments in one structured system.

If contractor payments are becoming difficult to manage, getting expert support can help you stay compliant and reduce admin.

Speak to Direct Payroll Services today for a quick assessment and set up a compliant, stress-free contractor payment process.

Conclusion

Managing contractor pay in the United Kingdom requires clarity across classification, IR35, and payment structure. Small mistakes can lead to compliance risks, penalties, and operational disruption. By choosing the right payment method, maintaining proper documentation, and following a structured process, businesses can reduce risk and improve efficiency.

As contractor relationships expand globally, having the right systems or payroll support in place ensures payments remain accurate, compliant, and easy to manage at scale.

Frequently Asked Questions

How do you pay international contractors securely?

Use trusted payment methods such as international wire transfers, global payroll providers, or verified digital payment platforms. Ensure proper contracts, clear payment terms, and compliance with local labour laws to reduce risk and protect both parties.

What is the best way to pay international contractors?

The best method depends on scale and location. For most businesses, global payroll systems or digital payment platforms offer a balance of speed, compliance, and cost efficiency compared to traditional bank transfers.

Do you need to withhold taxes when paying international contractors?

In most cases, UK businesses do not withhold tax for foreign contractors. However, tax obligations depend on the contractor’s home country and applicable tax treaties, so compliance checks are essential.

Can contractors be paid through payroll in the UK?

Yes, contractors can be paid through payroll if they fall inside IR35. In this case, tax and National Insurance must be deducted before payment, similar to employees.

What is contractor PAYE umbrella IR35?

It refers to a setup where contractors are paid through payroll or an umbrella company when IR35 applies, with taxes deducted at source to ensure compliance with HMRC regulations.

Are contractors entitled to sick pay in the UK?

No, contractor sick pay is not a statutory entitlement. Contractors are self-employed and responsible for managing their own income protection unless covered by specific umbrella arrangements.

What is the safest way to pay contractors?

The safest way is to use structured payment methods such as payroll systems, bank transfers, or regulated payment platforms, combined with clear contracts and proper classification to ensure compliance and reduce disputes.

How can I calculate the take-home pay for an international contractor?

To calculate take-home pay, start with the agreed rate, then factor in currency conversion, transaction fees, and any local taxes in the contractor’s home country. The final amount depends on local tax rules and the payment method used.

Are there recommended tools or calculators for estimating international contractor pay?

Yes, you can use global payroll calculators, currency conversion tools, and contractor rate estimators to get accurate figures. These tools help account for exchange rates, tax differences, and fees, giving a clearer estimate of final contractor earnings.