Key Highlights

- Payroll legislation governs how employers calculate pay, process deductions, and report payroll information to HMRC.

- Key compliance areas include PAYE, National Insurance contributions, workplace pensions, statutory payments, and IR35.

- Employers must meet RTI reporting obligations and maintain payroll records that support HMRC compliance.

- Statutory payments such as SSP, SMP, and SPP must be calculated using current eligibility rules and rates.

- Payroll deductions, tax codes, and pension contributions must be applied accurately to avoid reporting errors.

- Late payroll submissions and inaccurate reporting can lead to penalties, interest charges, and compliance reviews.

- Payroll errors can affect employee pay, create disputes, and increase administrative workload for employers.

- Regular payroll reviews and legislative monitoring help businesses maintain ongoing payroll compliance.

Payroll legislation is the framework of laws and regulations that govern how employers calculate, process, report, and pay employee wages in the UK. It covers key areas such as PAYE, National Insurance contributions, statutory payments, pensions, minimum wage requirements, and HMRC reporting obligations.

For employers, payroll legislation directly affects compliance, employee payments, and financial reporting. Failing to follow current payroll rules can lead to incorrect deductions, HMRC penalties, reporting errors, and disputes with employees, making it essential to keep payroll processes aligned with legal requirements.

This guide explains the key areas of UK payroll legislation, recent regulatory changes, employer responsibilities, common compliance risks, and the practical steps businesses can take to manage payroll accurately and remain compliant.

What Is Payroll Legislation in the UK?

Payroll legislation refers to the laws and regulations that govern how employers calculate pay, process deductions, report payroll information, and meet statutory payment obligations in the UK.

These rules help ensure employees are paid correctly while HMRC receives accurate tax and National Insurance contributions. They also govern workplace pensions, statutory payments, payroll reporting, and contractor tax compliance.

Key areas covered:

- PAYE tax deductions

- National Insurance contributions (NICs)

- Workplace pension auto-enrolment

- Statutory Sick Pay (SSP)

- Statutory Maternity Pay (SMP)

- Real Time Information (RTI) reporting

- Off-Payroll Working Rules (IR35)

Together, these areas form the foundation of payroll compliance and influence how employers calculate pay, manage deductions, report payroll information, and meet HMRC obligations throughout the tax year.

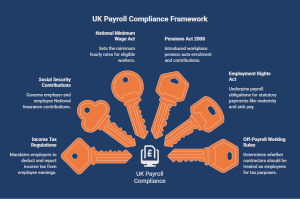

What Laws Govern Payroll in the UK?

UK payroll compliance is shaped by several laws that determine how employers calculate pay, deduct taxes, process pensions, administer statutory payments, and report payroll information to HMRC. Together, these regulations influence almost every stage of the payroll process.

- Income Tax (PAYE) Regulations:- PAYE regulations require employers to deduct income tax from employee earnings before wages are paid. They also set the rules for reporting tax deductions to HMRC through payroll submissions.

- Social Security Contributions Regulations:- These regulations govern employer and employee National Insurance contributions, including contribution thresholds, calculation methods, and reporting requirements.

- National Minimum Wage Act:- The National Minimum Wage Act sets the minimum hourly rates employers must pay eligible workers. Payroll systems must apply the correct rates to avoid underpayments and potential enforcement action.

- Pensions Act 2008:- This legislation introduced workplace pension auto-enrolment, requiring employers to enrol eligible employees into a pension scheme and make minimum pension contributions.

- Employment Rights Act:- The Employment Rights Act underpins payroll obligations linked to statutory payments, including maternity, paternity, adoption, and sick pay entitlements.

- Off-Payroll Working Rules (IR35):- IR35 rules help determine whether contractors should be treated as employees for tax purposes. Businesses engaging contractors must assess employment status carefully to ensure the correct tax treatment is applied.

Because these laws operate together, payroll compliance extends beyond salary calculations. Employers must ensure payroll processes, deductions, reporting, and employee entitlements remain aligned with current legal requirements throughout the tax year.

Why Must Employers Stay Compliant With Payroll Legislation?

Payroll compliance directly affects employee payments, tax reporting, and HMRC obligations. Incorrect PAYE deductions, missed pension contributions, underpayment of wages, or late RTI submissions can result in financial penalties, backdated payments, and additional scrutiny from HMRC.

The impact extends beyond compliance risks. Payroll errors can create employee disputes, damage trust, and increase administrative workload as businesses investigate discrepancies and correct payroll records. Maintaining compliance helps employers reduce reporting errors, meet statutory obligations, and ensure employees are paid accurately and on time.

What Are the New National Minimum Wage and Living Wage Rates?

National Minimum Wage (NMW) and National Living Wage (NLW) rates are reviewed annually and usually change from 1st April each year. Employers must apply the correct rates based on employee age and eligibility throughout the payroll year.

Although final 2026 rates may still be subject to government confirmation, employers should expect further increases following recent wage uplifts linked to inflation and cost-of-living pressures.

| Worker Category | Current Rate |

|---|---|

| National Living Wage (21+) | £11.44 |

| Ages 18–20 | £8.60 |

| Ages 16–17 | £6.40 |

| Apprentice Rate | £6.40 |

Even moderate wage increases can significantly affect businesses with large hourly-paid workforces. Employers should review:

- employee pay bands

- overtime calculations

- pension contribution costs

- salary sacrifice arrangements

- workforce budgets

Incorrect minimum wage payments remain one of the most common payroll compliance failures investigated by HMRC.

What Is the Difference Between the National Minimum Wage and the National Living Wage?

The National Living Wage applies to workers aged 21 and over, while the National Minimum Wage applies to younger employees and apprentices under different age-based pay bands.

Although both are statutory minimum pay requirements, the National Living Wage represents the highest legal hourly pay threshold. Employers must apply the correct rate based on employee age and apprenticeship status to remain compliant with wage legislation.

| Wage Type | Applies To |

|---|---|

| National Living Wage (NLW) | Employees aged 21 and over |

| National Minimum Wage (NMW) | Employees aged 16–20 and apprentices |

Both wage categories are reviewed annually by the Low Pay Commission and enforced through HMRC compliance monitoring.

What Are the Current Statutory Pay Rates for Employers?

Statutory pay rates are legally required payments employers must provide when eligible employees take leave for sickness, maternity, paternity, adoption, or shared parental responsibilities.

These payments must be processed through payroll and reported correctly to HMRC. Incorrect statutory pay calculations can lead to payroll corrections, employee disputes, and compliance issues, particularly when eligibility rules or payment thresholds are applied incorrectly.

Most statutory payment rates are reviewed annually before the new tax year. Employers should update payroll systems before April to ensure statutory pay calculations remain accurate across all payroll cycles.

| Statutory Payment Type | Weekly Rate |

|---|---|

| Statutory Sick Pay (SSP) | £116.75 |

| Statutory Maternity Pay (SMP) | £184.03 |

| Statutory Paternity Pay (SPP) | £184.03 |

| Statutory Adoption Pay (SAP) | £184.03 |

| Shared Parental Pay (ShPP) | £184.03 |

Because statutory payments affect both payroll costs and employee entitlements, businesses should regularly review payment eligibility, payroll calculations, and reporting accuracy throughout the tax year.

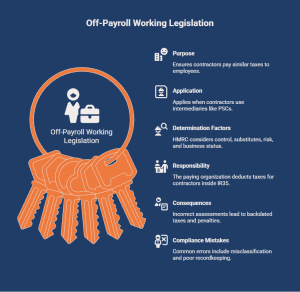

What Is Off-Payroll Working Legislation?

Off-payroll working legislation, commonly known as IR35, is designed to ensure contractors working in a similar way to employees pay broadly the same Income Tax and National Insurance contributions as permanent staff.

The rules apply when contractors provide services through intermediaries such as personal service companies (PSCs). Businesses must assess whether a contractor operates independently or works in a manner similar to an employee.

HMRC considers several factors when determining employment status, including:

- How much control the business has over the contractor’s work

- Whether the contractor can send a substitute to complete the work

- The level of financial risk carried by the contractor

- Whether the contractor works as an independent business or as part of the organisation

If a contractor is deemed to fall inside IR35, the organisation paying the contractor is generally responsible for deducting PAYE Income Tax and National Insurance contributions before payment is made.

Incorrect status assessments can result in backdated tax liabilities, penalties, and compliance investigations. Businesses that regularly engage contractors should review decisions on employment status carefully and maintain clear records to support their assessments.

What Are Common IR35 Compliance Mistakes?

Many off-payroll compliance issues occur when businesses rely solely on contract wording without reviewing actual working arrangements. HMRC assessments focus on how the contractor relationship operates in practice rather than what is written in the contract.

Common compliance mistakes include:

- misclassifying contractors as self-employed

- failing to issue a Status Determination Statement (SDS)

- using outdated contractor agreements

- applying inconsistent employment status assessments

- Inaccurate PAYE deductions for contractors inside IR35

- poor recordkeeping and documentation

Regular reviews of contractor arrangements can help businesses reduce tax risks and maintain compliance with off-payroll working rules.

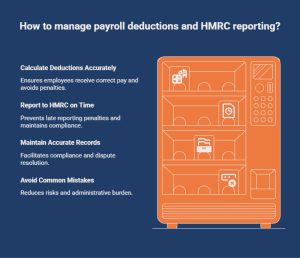

How Should Employers Manage Payroll Deductions and HMRC Reporting?

Payroll legislation places several legal responsibilities on employers. Businesses must calculate deductions correctly, submit payroll information to HMRC within required deadlines, maintain accurate payroll records, and ensure employees receive the correct pay and statutory entitlements. Failing to meet these obligations can result in penalties, payroll disputes, and additional compliance scrutiny.

What Payroll Deductions Are Employers Legally Required to Process?

Employers are responsible for applying statutory deductions accurately for every employee. These deductions must be calculated using the correct tax codes, contribution rates, and legal thresholds in force during the tax year.

| Payroll Deduction | Purpose |

|---|---|

| PAYE Income Tax | Employee tax contributions |

| National Insurance | State benefit contributions |

| Pension Contributions | Workplace pension funding |

| Student Loan Repayments | Loan recovery deductions |

| Attachment Orders | Court-ordered deductions |

Incorrect deductions can affect employee take-home pay, create PAYE discrepancies, and require payroll corrections. Employers must also ensure payroll systems are updated when HMRC changes tax codes, contribution thresholds, or deduction requirements.

What HMRC Reporting and Recordkeeping Requirements Must Employers Meet?

HMRC requires employers to report payroll information through the Real Time Information (RTI) system on or before each employee’s payday. Most payroll reporting is completed through a Full Payment Submission (FPS), while an Employer Payment Summary (EPS) may be required for payroll adjustments, statutory payment recoveries, or periods where employees have not been paid.

In addition to reporting obligations, employers must retain payroll records for the current tax year and at least three previous tax years. Records should include employee earnings, PAYE deductions, pension contributions, statutory payments, RTI submissions, and tax code information.

Accurate recordkeeping helps businesses demonstrate compliance, respond to HMRC enquiries, and resolve payroll disputes more efficiently.

What Are Common Payroll Compliance Mistakes and Their Consequences?

Many payroll compliance issues are caused by avoidable administrative errors rather than complex legislation. Common mistakes include applying incorrect tax codes, submitting RTI reports after payday, failing to update employee records, miscalculating pension contributions, or retaining incomplete payroll records.

These errors can have wider consequences than a simple payroll correction. HMRC may issue penalties for late reporting, charge interest on underpaid liabilities, or request additional information during compliance reviews. Repeated reporting issues can also increase administrative workload and create disputes when employees receive incorrect pay or deductions.

Regular payroll reviews, accurate recordkeeping, and timely HMRC reporting help employers reduce compliance risks and maintain payroll processes that remain aligned with current legislation.

What Happens If Payroll Reporting Is Late or Incorrect?

Late or inaccurate payroll reporting can lead to HMRC penalties, employee pay issues, payroll corrections, and increased compliance scrutiny. While a single reporting mistake may be resolved quickly, repeated errors can create wider financial and operational consequences for the business.

HMRC consequences

HMRC expects employers to submit payroll information accurately and on time through the Real Time Information (RTI) system. Late submissions, incorrect payroll reports, or unpaid PAYE liabilities can result in penalties, interest charges, and additional compliance checks.

| Payroll Compliance Issue | Potential Consequence |

|---|---|

| Late RTI submissions | Monthly HMRC penalties |

| Incorrect payroll reports | Compliance investigations |

| Late PAYE payments | Interest charges |

| National Minimum Wage underpayment | Financial penalties and enforcement action |

| Repeated payroll inaccuracies | Increased HMRC scrutiny |

Businesses that repeatedly miss reporting deadlines or submit inaccurate payroll data are more likely to face compliance reviews and requests for supporting payroll records.

Employee consequences

Payroll errors can affect employees immediately. Incorrect tax deductions, inaccurate pension contributions, underpayments, or delayed wages may create financial pressure and increase payroll-related complaints. Errors in payroll reporting can also affect employee tax records and statutory payment calculations, leading to further corrections later in the tax year.

Business consequences

Payroll reporting problems often create additional administrative workload. Employers may need to investigate discrepancies, process payroll corrections, amend HMRC submissions, and respond to employee queries. Repeated errors can reduce confidence in payroll processes, increase compliance risks, and divert time and resources away from other business activities.

Maintaining accurate payroll records, reviewing payroll calculations regularly, and meeting HMRC reporting deadlines can help businesses reduce these risks and avoid unnecessary compliance issues.

How Can Businesses Stay Compliant With UK Payroll Legislation?

Businesses stay compliant with UK payroll legislation by maintaining accurate payroll processes, monitoring legislative changes, and addressing reporting issues before they develop into recurring compliance problems. Consistent payroll reviews help employers identify errors early and keep payroll systems aligned with current requirements.

Payroll legislation changes regularly through updates to PAYE thresholds, National Minimum Wage rates, workplace pension requirements, statutory payments, and HMRC reporting rules. Monitoring HMRC guidance and payroll software updates helps businesses apply changes correctly and avoid reporting inaccuracies.

As payroll complexity grows, some employers choose to outsource payroll administration to reduce compliance risks. External payroll providers can support PAYE reporting, RTI submissions, pension administration, statutory payments, and ongoing legislative compliance, helping businesses maintain accurate payroll operations and meet HMRC obligations more consistently.

How Can Direct Payroll Services Help Businesses Manage Payroll Legislation?

Direct Payroll Services helps businesses manage payroll legislation through accurate payroll processing, RTI reporting, PAYE administration, pension management, and statutory payment support.

As payroll legislation changes, businesses must keep payroll systems up to date, maintain reporting accuracy, and consistently meet HMRC deadlines. Direct Payroll Services helps reduce compliance risks by supporting:

- PAYE payroll processing

- RTI submissions

- workplace pension administration

- statutory payments

- payroll deduction management

- contractor payroll support

For businesses managing growing payroll demands, outsourcing payroll can improve reporting accuracy, reduce administrative pressure, and help maintain compliance with changing UK payroll legislation.

Businesses looking to simplify payroll administration can explore support options through Direct Payroll Services.

Conclusion

UK payroll legislation continues to change as HMRC strengthens payroll reporting requirements, statutory payment rules, and PAYE compliance standards. Businesses must keep payroll systems updated, apply deductions accurately, maintain compliant payroll records, and submit RTI reports within required deadlines to avoid penalties and reporting issues.

Many payroll compliance problems develop through outdated payroll settings, missed legislative updates, or recurring reporting errors that remain unresolved across multiple pay cycles. Regular payroll reviews, accurate reporting procedures, and reliable payroll systems help businesses reduce compliance risks, improve payroll accuracy, and maintain smoother payroll operations throughout the tax year.

Frequently Asked Questions

What statutory changes are expected in UK payroll legislation for 2026?

UK payroll legislation changes in 2026 are expected to include updated minimum wage rates, revised statutory pay thresholds, pension contribution adjustments, and continued HMRC focus on RTI reporting accuracy and payroll compliance.

How can businesses stay informed on payroll compliance requirements?

Businesses can stay informed on payroll compliance requirements by monitoring HMRC updates, reviewing payroll software changes, following RTI reporting guidance, and regularly checking legislation affecting PAYE, pensions, statutory payments, and payroll deductions.

Where can I find up-to-date official guidance on UK payroll legislation?

Businesses can find official payroll legislation guidance on the GOV.UK website and through HMRC employer bulletins, which provide updates on PAYE reporting, statutory payments, pensions, and payroll compliance requirements.

How does payroll legislation differ across the devolved UK nations?

Most UK payroll legislation applies across England, Wales, Scotland, and Northern Ireland, but some tax rates and thresholds can differ. Scotland, for example, operates different Income Tax bands, which can affect PAYE calculations for Scottish taxpayers.

What penalties could businesses face for not following UK payroll legislation?

Businesses that fail to follow UK payroll legislation can face HMRC penalties, interest charges, compliance investigations, late filing fines, higher costs related to National Minimum Wage enforcement action, and payroll correction costs caused by inaccurate reporting or deductions.

How have recent employment law changes affected payroll processing in the UK?

Recent employment law changes have increased payroll complexity by introducing higher minimum wage rates, updated statutory payments, stricter RTI reporting expectations, and expanded pension compliance responsibilities, along with new regulations surrounding the secondary threshold. Businesses must now update payroll systems more frequently to maintain accurate reporting and deductions.

What are the main compliance requirements for running payroll in the UK?

The main UK payroll compliance requirements include accurate PAYE deductions, timely RTI submissions, correct pension contributions, statutory payment processing, payroll recordkeeping, compliance with National Minimum Wage, and claiming the increased employment allowance in HMRC reporting regulations.