Key Highlights

- An employment termination payment includes multiple components, each with different tax and NIC treatment

- Only genuine compensation qualifies for the £30,000 tax-free threshold under HMRC rules

- Earnings such as notice pay, bonuses, and unused leave are always fully taxable

- PENP rules ensure notice-related payments are treated as taxable income, not compensation

- NIC treatment differs from income tax, especially for compensation above £30,000

- Most payroll errors come from misclassification, not calculation, leading to compliance risks

Employment termination payments are one of the most error-prone areas in payroll.

It is rarely just one final payout. Notice pay, unused holiday, bonuses, and compensation can all be involved, each with different tax rules. This is where many employers run into issues. A small error in classification or calculation can lead to incorrect deductions, HMRC scrutiny, or disputes with a former employee.

The real challenge is knowing what should be taxed, what qualifies for relief, and how everything fits within the same tax year without creating compliance risks.

Understanding how termination payments work is essential for accuracy and compliance. This guide breaks down the rules, calculations, and HMRC treatment clearly, so you can handle payments correctly and avoid unnecessary risk.

What Is an Employment Termination Payment?

An employment termination payment refers to money paid to an employee when their employment ends. It may include contractual payments, such as salary, notice pay, and accrued holiday pay, as well as non-contractual compensation for loss of employment.

These payments can arise when an employee’s employment ends due to resignation, dismissal, redundancy, or a settlement agreement.

What Does It Include?

An employment termination payment may include:

- Final salary up to the date of termination

- Notice pay or payment instead of notice

- Accrued holiday pay or payment for untaken holiday

- Bonuses or commissions owed under the contract

- Statutory redundancy pay or severance compensation

Each component must be reviewed separately because the tax treatment depends on whether the payment is contractual earnings or compensation.

How Should Employers Classify Termination Payments?

Most payroll errors in the United Kingdom do not come from calculation. They come from misclassification.

A termination package often includes multiple components such as notice pay, holiday pay, or compensation. Treating these as one payment creates immediate compliance risk. Each element must be assessed separately before processing.

What Two Categories Do Termination Payments Fall Into?

Every termination payment falls into one of two categories, and this classification determines how it is taxed.

| Category | What It Means | Examples | Tax Treatment |

|---|---|---|---|

| Earnings | Payments that arise from the contract of employment | Salary, notice pay, and accrued holiday pay | Fully taxable |

| Compensation | Payments are made because the employment has ended, not for work performed | Redundancy pay, severance, ex gratia payments | May be tax-free (up to £30,000) |

Why This Decision Matters?

Getting this step right determines everything that follows:

- Whether the payment is taxable under HMRC rules

- Whether NICs apply

- How the payment is processed through payroll

- How it is reported to HMRC

Even when paid together, each component must be split and classified correctly. This is the foundation of compliant payroll processing.

When Is a Termination Payment Taxable in the UK?

A termination payment is taxable when it is treated as earnings or when compensation exceeds the £30,000 tax-free threshold.

The key for employers is identifying which elements fall under taxable earnings and ensuring they are processed correctly through payroll.

Fully Taxable Components

The following elements are always treated as earnings and must be processed through PAYE:

- Salary up to the final working day

- Notice pay, including Post-Employment Notice Pay (PENP)

- Bonuses and commissions

- Accrued holiday pay (unused annual leave)

- Sick pay, where applicable

These payments are taxed in the relevant tax year, with both income tax and National Insurance applied in full.

Which Termination Payments Can Be Tax-Free?

Not all termination payments are taxable. Certain compensation payments can qualify for tax relief, but only when they meet strict HMRC conditions.

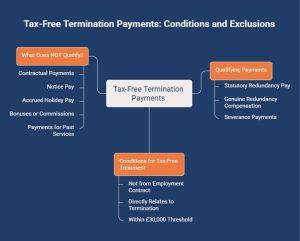

1. Qualifying Payments

The following may be tax-free up to £30,000:

- Statutory redundancy pay

- Genuine redundancy compensation

- Severance payments not linked to contractual obligations

These payments must reflect compensation for loss of employment rather than payment for work done.

2. Conditions for Tax-Free Treatment

To qualify for exemption:

- The payment must not arise from the employment contract

- It must directly relate to the termination of employment

- The total must remain within the £30,000 threshold

Any amount above this limit becomes taxable and must be processed through PAYE.

What Does NOT Qualify for Tax-Free Treatment?

The following do not qualify for the £30,000 exemption, even if paid at termination:

- Payments that are contractual under the employment agreement

- Notice pay, including Post-Employment Notice Pay (PENP)

- Accrued holiday pay or unused annual leave

- Bonuses or commissions linked to performance

- Payments for services performed before the last day of employment

These are treated as earnings, not compensation, and are fully taxable.

The key is to separate compensation from earnings. Once that line is blurred, tax exposure increases quickly.

How Does PENP Affect Notice Pay?

Post-Employment Notice Pay (PENP) ensures that any payment linked to an unworked notice period is treated as earnings and taxed through PAYE.

When Does PENP Apply?

PENP applies when an employee does not work all or part of their notice period, including:

- Payment in lieu of notice (PILON)

- Immediate termination without working notice

- Partially worked notice periods

In all cases, the unworked portion is treated as taxable income.

How Is PENP Calculated?

PENP = Pay for the unworked notice period

This amount must be processed as earnings within the relevant tax year.

PENP Examples

Example 1: Full PILON

- Salary: £3,000/month

- Notice: 2 months

PENP = £6,000 → fully taxable

Example 2: Partial Notice Worked

- Salary: £3,000/month

- 1 month worked, 1 month unpaid

PENP = £3,000 → taxable

Example 3: PILON + Compensation

- Salary: £4,000

- £4,000 PILON + £10,000 severance

£4,000 taxable, £10,000 may be tax-free

This means labels do not change tax treatment. If the payment relates to notice, it will be taxed accordingly.

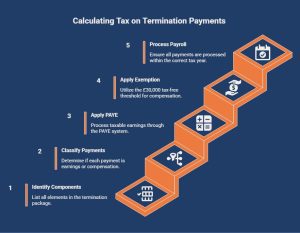

How Should Employers Approach Calculating Tax on Termination Payments?

Calculating tax on termination payments requires a structured approach, as each component is treated differently under HMRC rules. Treating the entire payment as one amount often leads to errors, making it essential to break down and assess each element carefully.

Step 1: Identify All Components in the Final Pay

The process begins by outlining every element included in the termination package. This typically includes final salary, notice pay, bonuses, unused leave, and any redundancy or compensation payments.

Step 2: Classify Each Payment

Once identified, each component must be classified correctly. Payments are either treated as earnings or as compensation, which determines whether they are fully taxable or eligible for tax relief.

Step 3: Apply PAYE to Taxable Elements

All payments classified as earnings must be processed through PAYE. This includes salary, notice pay, and other contractual payments, with income tax and National Insurance applied accordingly.

Step 4: Apply the £30,000 Exemption

Qualifying compensation payments can be paid tax-free up to £30,000 if they meet HMRC conditions. Any amount above this threshold becomes taxable and must be processed through payroll.

Step 5: Process Payroll Within the Correct Tax Year

All termination payments must be processed within the correct tax year to ensure accurate reporting and compliance with HMRC requirements.

Worked Example: Full Termination Payment Breakdown

Scenario:

An employee’s employment ends on 30th April with the following package:

- Monthly salary: £3,000

- Unworked notice period: 2 months

- Unused annual leave: £1,500

- Bonus: £2,000

- Redundancy compensation: £20,000

Step 1: Classification

| Component | Amount | Classification | Tax Treatment |

|---|---|---|---|

| Final salary | £3,000 | Earnings | Fully taxable |

| Notice pay (PENP) | £6,000 | Earnings | Fully taxable |

| Unused annual leave | £1,500 | Earnings | Fully taxable |

| Bonus | £2,000 | Earnings | Fully taxable |

| Redundancy compensation | £20,000 | Compensation | Tax-free (within £30,000) |

Step 2: Apply Tax

- Total taxable earnings:

£3,000 + £6,000 + £1,500 + £2,000 = £12,500

→ Subject to PAYE and National Insurance - Tax-free compensation:

£20,000 → No tax applied (within £30,000 threshold)

Final Outcome

- Total payment: £32,500

- Taxable amount: £12,500

- Tax-free amount: £20,000

Only the portion classified as earnings is taxable. Breaking down each component ensures accurate deductions and prevents HMRC compliance issues.

Not sure how holiday pay works for casual workers? Understand how to calculate entitlements correctly and avoid common payroll mistakes.

What Is the NIC Treatment of Termination Payments?

National Insurance Contributions do not always follow the same logic as income tax when it comes to termination payments. This is where payroll teams often make mistakes, especially when different components such as earnings and compensation are involved. Understanding how NIC applies helps ensure accurate deductions and avoid compliance risks.

Which Elements Are Subject to Full NIC?

Payments treated as earnings are fully subject to NIC, including:

- Salary

- Notice pay (including PENP)

- Bonuses

- Accrued holiday pay

These are processed through payroll with both employee and employer NIC applied.

When Does Employer NIC Apply to Compensation?

Since April 2020, employer NIC applies to any portion of termination payments that exceeds £30,000.

This means:

- Compensation up to £30,000 → No NIC

- Compensation above £30,000 → Employer NIC applies (Class 1A)

- Employee NIC → Not applied to compensation

This rule is often missed, leading to underreported employer costs.

Are Any Termination Payments Exempt From NIC?

Some compensation payments are exempt from employee NIC, particularly those within the £30,000 threshold.

However, treatment depends on correct classification. If a payment is treated as earnings, full NIC applies regardless of timing or structure.

NIC treatment depends on whether a payment is classified as earnings or compensation.

Since April 2020, employers must account for NIC on compensation above £30,000, even when employee NIC does not apply.

Managing temporary staff payroll can be just as complex as termination payments. Learn how to stay compliant and avoid common payroll errors.

What Do Termination Payments HMRC Rules Require?

Termination payments HMRC rules are primarily governed by the Income Tax (Earnings and Pensions) Act 2003 (ITEPA), particularly Section 401, which covers payments made in connection with the termination of employment.

HMRC guidelines focus on how termination payments are structured, classified, and reported. Simply labelling a payment as compensation is not enough. Employers must apply the correct tax treatment based on the nature of each payment.

How Should Termination Payments Be Processed?

All relevant payments must be processed through PAYE and reported via Real Time Information (RTI). This ensures that tax and National Insurance are applied correctly at the point of payment.

What Are the Key Compliance Requirements?

Employers must:

- Apply correct tax and NIC deductions

- Classify each component accurately

- Maintain clear documentation for audit purposes

- Ensure treatment aligns with ITEPA 2003 Section 401 rules

Accurate records are essential to demonstrate compliance if reviewed by HMRC.

Why Does Classification Matter More Than Labelling?

HMRC assesses the substance of the payment rather than its description. Even if a payment is labelled as compensation, it may still be treated as earnings if it relates to contractual obligations.

Incorrect classification can lead to underpaid tax, reporting errors, and potential penalties.

ITEPA 2003 Section 401 requires employers to assess termination payments based on their true nature, not their label.

Applying these rules correctly ensures compliance and reduces the risk of HMRC challenges.

What Are the Most Common Employer Mistakes?

Errors in termination payments are rarely caused by system failures. They are usually the result of misunderstanding rules or applying incorrect assumptions during processing.

1. Why Do Employers Treat Payments as Tax-Free?

A common mistake is assuming all termination payments fall within the £30,000 tax-free threshold. In reality, only qualifying compensation is exempt. Earnings elements remain fully taxable.

2. How Is Notice Pay Often Misclassified?

Post-Employment Notice Pay (PENP) is frequently misunderstood. Employers may treat it as compensation when it should be taxed as earnings, leading to incorrect deductions.

3. What Happens When PENP Rules Are Ignored?

Ignoring PENP rules can result in underpaid tax and National Insurance, increasing the risk of HMRC scrutiny and penalties.

4. How Are Settlement Agreements Misclassified?

Payments made under settlement agreements are often assumed to be tax-free. However, the tax treatment depends on what the payment represents, not the agreement itself.

If any part relates to:

- Notice pay

- Bonuses or contractual entitlements

- Payments for services

It will be treated as earnings and taxed accordingly.

5. Why Is Documentation Often Overlooked?

Incomplete or unclear records make it difficult to justify classification decisions. This increases the risk of disputes, especially with a former employee, and creates compliance challenges.

Most errors come from misclassification, not calculation. Clear separation of earnings and compensation, supported by proper documentation, is essential for compliance.

Think you’ve got payroll figured out? Some of the most common payroll myths still catch businesses off guard.

When Should You Seek Payroll or Legal Advice?

Not all termination payments are straightforward. Certain scenarios involve higher complexity and risk, making professional guidance essential.

Which Situations Require Expert Input?

You should seek support in cases involving:

- Redundancy programmes

- Settlement agreements

- Director or senior executive exits

- Tribunal risk or ongoing disputes

These situations often involve multiple payment components, legal exposure, and higher financial impact.

How Do International Elements Increase Risk?

Payments involving foreign service or cross-border employees require careful handling due to differing tax rules and reporting requirements.

Why Is Combined Payroll and Legal Support Important?

Payroll ensures accurate calculation, classification, and HMRC compliance, while legal advice helps structure agreements correctly and reduce exposure to disputes or tribunal claims.

Complex termination scenarios require both payroll accuracy and legal clarity. Getting expert input early helps prevent costly errors and compliance risks.

How Direct Payroll Services Help You Handle Termination Payments?

Termination payments often go wrong at the classification stage, leading to incorrect tax treatment, NIC errors, and compliance risks.

Direct Payroll Services helps businesses across the United Kingdom manage this accurately by:

- Correctly splitting earnings and compensation components

- Applying PENP rules to notice pay without errors

- Handling PAYE and NIC calculations in line with HMRC rules

- Processing and reporting payments through RTI

- Supporting complex cases such as redundancy and settlement agreements

This ensures termination payments are accurate, compliant, and processed without unnecessary risk.

Speak to Direct Payroll Services to handle termination payments with confidence and full compliance.

Conclusion

Employment termination payments are not about processing a final figure, but making the right decisions at each step. The real risk lies in misjudging how individual components should be treated, especially under time pressure or complex exit scenarios.

Clear structure, accurate handling, and timely reporting make the difference between smooth processing and costly errors. For organisations managing high-value or sensitive exits, expert support helps ensure everything is handled correctly the first time.

Frequently Asked Questions

Which parts of a termination payment are taxable?

Payments treated as earnings, such as notice pay, salary, bonuses, and unused holiday pay, are fully taxable. Compensation payments may be tax-free up to £30,000 if they meet HMRC conditions.

How do employers calculate tax on termination payments?

Employers must separate each component, classify it as earnings or compensation, apply PAYE to taxable elements, and then apply the £30,000 exemption to qualifying payments before processing payroll.

Are redundancy payments different from other termination payments?

Yes, redundancy payments are a type of termination payment. Genuine redundancy compensation can qualify for the £30,000 tax-free threshold, unlike contractual payments such as notice pay, which are always taxable.

What compliance steps must employers follow for termination payments?

Employers must correctly classify payments, apply PAYE and NIC where required, report through RTI, maintain proper documentation, and follow HMRC and ITEPA rules to avoid penalties or disputes.

Is an eligible termination payment used in the UK?

No. This term is used in other jurisdictions. In the UK, HMRC assesses termination payments based on classification rules under ITEPA.

Is PILON taxable?

Yes. Payment in lieu of notice (PILON) is treated as earnings under HMRC rules. It is fully taxable through PAYE and subject to National Insurance, regardless of how it is structured or described in the agreement.

Is the settlement agreement compensation tax-free?

Not always. Only the portion that qualifies as compensation for loss of employment may be tax-free up to £30,000. Any amount linked to earnings, notice pay, or contractual entitlements remains fully taxable.

Is redundancy pay taxable?

Statutory redundancy pay is usually tax-free up to £30,000. However, any excess above this threshold becomes taxable. Enhanced redundancy payments follow the same rule if they qualify as genuine compensation.

Can notice pay be tax-free?

No. Notice pay, including Post-Employment Notice Pay (PENP), is always treated as earnings. It is fully taxable and subject to National Insurance, even if it is included within a termination payment package.

Is holiday pay included in termination pay?

Yes. Accrued or unused holiday pay is included in termination pay. It is treated as earnings, meaning it is fully taxable and subject to PAYE and National Insurance contributions.

Does the employer NIC apply above £30,000?

Yes. Since April 2020, employer National Insurance applies to any portion of termination payments exceeding £30,000. Employee NIC does not apply to this excess, but employer NIC must still be paid.