Key Highlights

Here are the key takeaways from our guide on calculating weekly pay:

- Weekly pay is calculated using gross earnings, additional income, and statutory deductions

- Gross pay forms the base, while overtime and bonuses increase total earnings

- PAYE deductions include income tax, National Insurance, and other statutory contributions

- Net pay represents the final take-home amount after all deductions

- Payroll adjustments can change weekly pay due to overtime, absences, or corrections

- Different pay structures affect how weekly earnings are calculated and vary in consistency

- Accurate payroll processes are essential to avoid errors, disputes, and compliance risks

- Clear communication and detailed payslips help employees understand their earnings

Weekly pay calculations often seem straightforward, but errors are common when dealing with variable hours, overtime, and changing deductions. Even small mistakes can lead to underpayments, payroll disputes, and compliance issues with HMRC.

For UK businesses, inaccurate weekly pay doesn’t just affect employees; it can result in penalties, reporting errors, and loss of trust. Applying PAYE correctly, managing deductions, and ensuring minimum wage compliance requires a structured and consistent approach every pay cycle.

This guide explains how to calculate weekly pay step by step, covering gross pay, deductions, tax calculations, and real-world scenarios. It also outlines common risks and the practical actions employers can take to ensure accuracy and maintain compliance.

What Should You Know About Weekly Pay in the UK?

Weekly pay is a payroll structure where employees are paid every seven days based on actual hours worked or fixed weekly earnings.

Unlike monthly payroll, weekly pay reflects real-time earnings, making it more suitable for hourly, shift-based, or variable-hour roles. This means pay can change each week depending on hours worked, overtime, or absences, rather than remaining fixed.

In addition to regular wages, a “week’s pay” is also used as a legal benchmark for calculating statutory payments such as redundancy pay and holiday pay. This applies even to employees who are not paid weekly, making it an essential concept across all payroll structures.

All weekly payroll calculations must align with HMRC requirements, ensuring that earnings and statutory payments are calculated correctly and consistently.

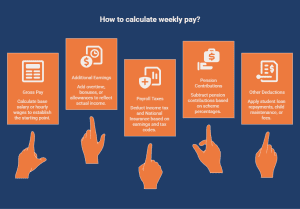

What Components Are Included in Weekly Pay Calculations?

Weekly pay is calculated by combining gross earnings, additional income, and deductions to determine final take-home pay. Gross pay is the starting point, including basic salary or hourly wages. Additional earnings, such as overtime or bonuses, increase total pay, while deductions like income tax, National Insurance, and pension contributions reduce it.

Understanding how each stage connects ensures accurate payroll calculations and a clear breakdown of weekly earnings.

1. Gross Pay

Gross pay is the starting point of the calculation and represents total earnings before deductions.

For salaried employees, this is calculated by dividing annual salary by 52. For hourly workers, it is based on hours worked multiplied by the agreed hourly rate.

This figure forms the base to which all additional earnings are added.

2. Overtime and Additional Earnings

Once gross pay is established, any additional earnings are added to calculate total weekly income.

These may include:

- Overtime payments

- Bonuses or commission

- Shift allowances

- Statutory payments such as sick pay

Adding these ensures the calculation reflects actual earnings for that pay period.

3. Payroll Taxes (PAYE)

After total earnings are calculated, statutory deductions are applied through the PAYE system. Income tax and National Insurance are calculated based on earnings and tax codes, and deducted before payment. These deductions reduce total earnings to determine the taxable net amount.

4. Pension Contributions

Following tax deductions, pension contributions are applied based on employee and employer schemes.

These are typically calculated as a percentage of earnings and deducted automatically through payroll. In some cases, salary sacrifice arrangements may adjust taxable income before deductions are applied.

5. Other Deductions

Finally, any additional deductions are applied to arrive at the final net pay.

Common examples include:

- Student loan repayments

- Child maintenance

- Salary sacrifice arrangements

- Union or membership fees

Each of these reduces the final amount an employee receives.

Together, these components determine how weekly earnings are calculated, ensuring payroll accuracy, compliance, and a clear understanding of take-home pay.

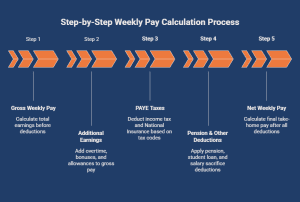

How to Calculate Weekly Pay Step-by-Step?

Weekly pay is calculated by determining total earnings for the week and applying all statutory and personal deductions to arrive at net pay.

While the steps are straightforward, most payroll errors happen during execution, especially with variable hours, incorrect rates, or missed deductions. Following a structured process with built-in checks helps ensure accuracy and compliance with HMRC requirements.

Step 1: Determine Gross Weekly Pay

Gross weekly pay is the total earnings before deductions and forms the base for all calculations.

For salaried employees, divide the annual salary by 52. For hourly workers, multiply hours worked by the agreed rate.

Where errors happen:

- Incorrect hours logged (especially shifts/overtime)

- Outdated hourly rates or pay increases have not been applied

- Missing adjustments for unpaid leave

What to double-check:

- Timesheets match actual worked hours

- Pay rates reflect current contracts and legal minimums

- Any pay changes are applied from the correct date

Accuracy at this stage is critical, as all taxes and deductions are applied to this amount, and employers must ensure pay rates meet current legal requirements, including recent updates such as the minimum wage increase for 2026.

Step 2: Add Additional Earnings

Additional earnings must be added to reflect total weekly income. This includes overtime, bonuses, commission, and allowances.

Where errors happen:

- Overtime calculated at the wrong rate

- Bonuses missed or applied in the wrong pay period

- Inconsistent recording of shift allowances

What to double-check:

- Overtime rates match contract terms

- All variable earnings are recorded before payroll is processed

- One-off payments are assigned to the correct week

These additions directly affect taxable income, so accuracy is essential before moving to deductions.

Step 3: Calculate PAYE Taxes

PAYE deductions include income tax and National Insurance based on earnings and tax codes. Employers apply these automatically through payroll systems.

Where errors happen:

- Incorrect or outdated tax codes

- Wrong NI thresholds applied

- System misalignment after pay changes

What to double-check:

- Tax code matches HMRC records

- Thresholds and rates are updated for the current tax year

- Deductions align with payslip expectations

Errors at this stage can lead to compliance issues and HMRC corrections.

Step 4: Deduct Pension & Other Deductions

After taxes, additional deductions are applied based on employee-specific arrangements. These include pensions, student loans, and salary sacrifice schemes.

Where errors happen:

- Pension percentages applied incorrectly

- Missing student loan deductions

- Salary sacrifice not reflected in taxable income

What to double-check:

- Contribution rates match employee agreements

- All deductions are correctly configured in payroll systems

- Salary sacrifice impacts are applied before tax calculations

Each deduction directly reduces net pay and must be recorded clearly.

Step 5: Calculate Net Weekly Pay

Net pay is the final amount received after all deductions are applied.

Formula: Gross Pay – Total Deductions = Net Weekly Pay

Where errors happen:

- Missing deductions or double deductions

- Incorrect final calculations

- Rounding errors in payroll systems

What to double-check:

- Final net pay matches the payslip breakdown

- All deductions are accounted for once

- No discrepancies between system output and manual checks

Quick Checklist Before Final Calculation

Before finalising weekly pay, run through this quick check to avoid common payroll errors:

- Confirm that all hours worked are verified and approved

- Check that hourly rates and salary figures are up to date

- Ensure overtime, bonuses, and allowances are fully included

- Verify tax codes and National Insurance thresholds are correct

- Confirm pension contributions and other deductions are applied accurately

- Check for any missing or duplicate deductions

- Compare net pay against the expected payslip breakdown

Running this final check helps prevent errors, ensures compliance, and reduces the need for payroll corrections after processing.

This figure represents the actual take-home pay and is the most important for budgeting and financial planning. Accurate calculations at this stage ensure employees are paid correctly and that payroll records remain compliant.

What Does a Weekly Pay Calculation Example Look Like?

A hypothetical example helps demonstrate how weekly earnings are calculated from gross pay to final take-home pay. Consider an employee earning £12 per hour, working standard weekly hours, along with some overtime paid at a higher rate. The example below shows how total earnings and deductions are applied.

| Description | Calculation | Amount (£) |

|---|---|---|

| Normal Pay | 37.5 × £12 | 450.00 |

| Overtime Pay | 5 × £18 | 90.00 |

| Gross Weekly Pay | 450 + 90 | 540.00 |

| Income Tax | Example deduction | -49.60 |

| National Insurance | Example deduction | -35.76 |

| Pension (5%) | Example deduction | -27.00 |

| Net Weekly Pay | 540 – deductions | 427.64 |

Note: This hypothetical breakdown shows how additional earnings increase gross pay, while deductions determine the final net amount received.

What This Example Shows

- Impact of overtime:

The additional 5 overtime hours increase gross pay by £90, showing how extra hours directly boost total earnings. - Deductions reduce take-home pay:

From £540 gross pay, £112.36 is deducted, leaving £427.64 as net pay. - Percentage lost in deductions:

Around 20.8% of total earnings is deducted through tax, National Insurance, and pension contributions.

This example highlights how both earnings and deductions directly influence take-home pay, making it essential to calculate each component accurately to avoid discrepancies.

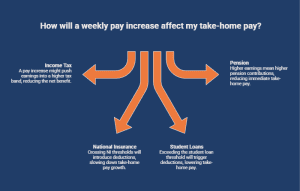

How Are Weekly Payroll Taxes Calculated in the UK?

Weekly payroll taxes are calculated based on earnings thresholds, meaning deductions increase as weekly pay rises.

Rather than focusing on tax rules alone, the key is understanding how crossing certain earnings thresholds affects take-home pay each week. Even small increases in earnings can lead to higher deductions depending on thresholds.

1. Income Tax Bands

Income tax increases as weekly earnings move beyond the tax-free and basic rate thresholds.

- If earnings fall within the Personal Allowance, no tax is deducted

- Once earnings exceed this threshold, tax is applied at increasing rates

Example:

If weekly earnings increase due to overtime, a portion of that extra income may fall into a taxable band, reducing the net benefit of higher pay.

2. National Insurance

National Insurance is applied only after weekly earnings cross specific thresholds.

- No NI is paid below the lower threshold

- A standard percentage applies within the main earning band

- A lower rate applies to higher earnings above the upper threshold

Example:

An employee earning slightly above the NI threshold will start seeing deductions, meaning take-home pay increases more slowly than gross pay.

3. Student Loans

Student loan deductions apply only when weekly earnings exceed the repayment threshold.

- No deductions below the threshold

- A fixed percentage applies to earnings above it

Example:

A small pay increase can trigger student loan deductions, reducing the overall increase in take-home pay.

4. Pension

Pension deductions are typically a percentage of earnings, increasing as pay rises.

- Higher earnings lead to higher contributions

- Salary sacrifice schemes may reduce taxable income before deductions

Example:

An increase in weekly earnings results in higher pension contributions, slightly lowering immediate take-home pay.

Understanding how these thresholds affect deductions helps explain why increases in gross pay do not always translate directly into higher take-home pay.

You can also explore this guide on salary sacrifice pension tax relief to understand how these arrangements affect taxable income and weekly pay calculations.

How Do Payroll Adjustments Affect Weekly Pay?

Payroll adjustments change weekly pay by altering either gross earnings or deductions within a specific pay period. These adjustments often occur when employee circumstances or payroll data change. For example, updates to tax codes can increase or reduce deductions, while corrections to previous errors may result in additional or reduced pay in the following week.

Common adjustments include:

- Backdated pay rises or corrections:- These increase gross pay in a later period to correct previous underpayments.

Impact: Can result in higher deductions in the same week due to increased taxable income. - Changes in overtime or working hours:- Weekly pay fluctuates based on actual hours worked.

Impact: Higher hours increase earnings but may also push income into higher deduction thresholds. - New or revised allowances:- Includes shift allowances or role-based payments.

Impact: Increases gross pay but may affect tax and National Insurance calculations. - Absence or unpaid leave deductions:- Reductions are applied when employees work fewer hours.

Impact: Lowers gross pay, which may also reduce tax and NI deductions.

Because weekly payroll reflects real-time changes, even small adjustments can affect take-home pay. Reviewing payslips regularly helps ensure accuracy and allows both employers and employees to identify and address discrepancies quickly.

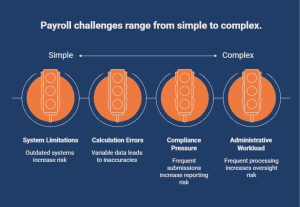

What Payroll Challenges Do Businesses Face When Calculating Weekly Pay?

Weekly payroll introduces operational complexity, where frequent calculations increase the risk of errors, compliance pressure, and system limitations.

Unlike less frequent payroll cycles, weekly processing requires constant updates to hours, earnings, and deductions. This creates multiple points where inaccuracies can occur if processes are not tightly controlled.

Key Payroll Challenges

- Calculation errors due to variable data:- Weekly payroll relies on changing inputs such as hours worked, overtime, and adjustments.

Challenge: Even small data entry errors can lead to incorrect pay and require reprocessing. - Compliance pressure with HMRC requirements:- Frequent payroll submissions increase the risk of reporting inaccuracies.

Challenge: Incorrect tax, National Insurance, or reporting data can result in penalties and corrections. - System limitations and manual processes:- Businesses relying on outdated systems or spreadsheets face a higher risk.

Challenge: A lack of automation increases the risk of missed deductions or incorrect calculations. - High administrative workload: processing weekly payroll increases operational demand.

Challenge: Payroll teams must handle calculations, checks, and reporting more frequently, increasing the likelihood of oversight.

Managing these challenges requires structured processes, accurate data handling, and reliable payroll systems to ensure consistent and compliant weekly pay calculations.

What Are the Risks of Incorrect Weekly Pay Calculations?

Incorrect weekly pay calculations don’t just create errors, they trigger operational, financial, and compliance risks that compound over time.

While payroll mistakes can happen in any business, weekly payroll increases exposure due to the frequency of calculations and reporting. Small errors repeated across multiple pay cycles can quickly escalate into larger issues.

Where the Real Risk Lies

- Repeated small errors: Minor miscalculations in hours, overtime, or deductions may seem insignificant.

Risk: When repeated weekly, they lead to cumulative underpayments or overpayments. - Incorrect deductions and reporting: Errors in tax or National Insurance calculations affect payroll records.

Risk: Can trigger HMRC corrections, penalties, or compliance reviews. - Payroll corrections and reprocessing: Fixing mistakes requires time and resources.

Risk: Increases administrative workload and delays payroll accuracy. - Employee dissatisfaction and disputes: Inconsistent pay creates confusion and mistrust.

Risk: Leads to complaints, disputes, and reduced employee confidence.

Most Common Risk in Small Businesses

Small businesses often rely on manual processes or limited payroll systems. The biggest risk is inconsistent data handling, such as incorrect hours, outdated pay rates, or missed deductions, which leads to recurring payroll errors across multiple weeks. Without structured checks, these errors are harder to detect early and more costly to correct later.

Managing these risks requires consistent payroll processes, accurate data inputs, and regular checks to ensure weekly pay calculations remain reliable and compliant.

What Should Employers Do to Ensure Accurate Weekly Pay?

Employers should follow structured payroll processes, use reliable systems, and maintain accurate records to ensure weekly pay is calculated correctly.

Using payroll software helps automate calculations for PAYE, National Insurance, pensions, and other deductions, reducing manual errors. Employers should also keep employee data up to date, including tax codes, pay rates, and working hours.

Key actions include:

- Verifying hours worked and additional earnings

- Applying correct tax codes and deduction rates

- Reviewing payroll calculations before processing

- Keeping up with HMRC rules and updates

A consistent and controlled approach ensures accuracy, compliance, and timely payments every pay cycle.

How Does Weekly Pay Impact Business Operations?

Weekly pay affects payroll workload, cash flow, and employee satisfaction. Processing payroll every week increases administrative effort and requires consistent accuracy. However, it can improve employee morale by providing regular income, especially for hourly workers, making effective payroll management essential.

| Area | Positive Impact | Operational Challenge |

|---|---|---|

| Employee Satisfaction | More frequent pay improves morale and retention | — |

| Financial Stability (Employees) | Helps employees manage weekly expenses better | — |

| Payroll Processing | — | Increased frequency of payroll runs |

| Administrative Workload | — | Higher workload for payroll teams |

| Cash Flow Management | — | Requires consistent weekly cash availability |

| Error Risk | — | More frequent processing increases risk of mistakes |

Weekly pay can improve workforce satisfaction, but it requires efficient payroll systems and strong financial planning to manage operational demands effectively.

When Weekly Pay Works Best

- Businesses with hourly or shift-based workers

- Industries with high staff turnover (e.g., hospitality, retail)

- Workforces that rely on frequent income for budgeting

When Weekly Pay May Not Be Suitable

- Businesses with limited payroll resources or manual systems

- Organisations with stable, salaried workforces

- Companies need tighter cash flow control

Weekly pay can improve employee experience, but without efficient payroll systems and strong processes, it can increase operational pressure and risk.

Why Choose Direct Payroll Services for Weekly Pay Management?

For many businesses, managing weekly payroll in-house can become increasingly complex, especially with variable hours, frequent calculations, and ongoing compliance requirements.

Professional payroll providers such as Direct Payroll Services support businesses by handling weekly payroll processing, PAYE calculations, pension contributions, and HMRC reporting. This ensures accurate calculations, timely payments, and full visibility across every pay cycle.

Outsourcing weekly payroll reduces administrative workload while maintaining accuracy and compliance with UK employment and tax regulations. It also provides scalable solutions that adapt to changing workforce needs and pay structures.

Looking for reliable weekly payroll support? Get in touch with Direct Payroll Services today.

Conclusion

Calculating weekly pay requires more than basic arithmetic. It involves understanding earnings structures, applying statutory deductions correctly, and managing ongoing payroll changes. Each step, from gross pay to final net pay, plays a critical role in ensuring employees are paid accurately.

For businesses, maintaining accuracy is essential to avoid compliance risks and operational challenges. Implementing structured payroll processes and using reliable systems can significantly reduce errors. A consistent approach not only improves efficiency but also builds trust, ensuring employees have confidence in how their pay is calculated.

Frequently Asked Questions

What deductions are taken from my weekly pay in the UK?

Income tax, National Insurance, pension contributions, and student loan repayments are commonly deducted from weekly pay. Additional deductions may include salary sacrifice schemes, child maintenance, or union fees, depending on individual circumstances and employment agreements.

How do gross and net weekly pay differ?

Gross weekly pay is the total earnings before deductions, while net weekly pay is the final amount received after subtracting income tax, National Insurance, pension contributions, and other deductions.

How are tax and National Insurance deducted from my weekly pay?

Income tax and National Insurance are deducted through the PAYE system. Employers calculate these based on your earnings, tax code, and weekly thresholds, then subtract them from your gross pay before issuing your net weekly pay, including such benefits.

What information do I need to calculate my weekly pay manually?

You need your pay rate (salary or hourly), hours worked, any additional earnings (overtime or bonuses), tax code, and details of deductions such as income tax in England, National Insurance, pension, and student loan repayments.

How can I use an online calculator to find my weekly take-home pay?

Enter your salary or hourly rate, number of hours worked, tax code, and deductions (pension, student loan) into an online salary calculator. It automatically applies PAYE rules to accurately estimate your weekly net pay.