Key Highlights

- How to calculate monthly payroll begins with determining gross pay, including salary and any additional earnings such as overtime or bonuses.

- Payroll is processed through the PAYE system, where income tax and National Insurance are calculated using tax codes, rates, and thresholds.

- Statutory deductions are applied first, followed by pension contributions and other employee-specific deductions.

- Payroll adjustments, such as mid-month starters, leavers, or unpaid leave, are applied to earnings before final calculations.

- Net pay is calculated after all deductions, ensuring the correct amount is paid to employees.

- Payroll schedules can influence how pay and adjustments are calculated across different pay periods.

- Many businesses use payroll providers to improve accuracy, ensure compliance, and streamline payroll processing.

For businesses in the United Kingdom, payroll is far more than simply paying employees each month; it is a high-stakes process where even minor errors can lead to compliance risks, financial penalties, and employee dissatisfaction. From calculating earnings and applying statutory deductions to maintaining HMRC-compliant records, every step must be precise, timely, and fully aligned with current regulations.

Although many organisations use monthly payroll for salaried roles, calculations can become complex. Over time, taxes, pensions, and deductions must all be processed accurately to avoid payment errors or compliance issues.

Understanding monthly payroll helps businesses stay compliant and pay employees correctly. This guide explains the key elements of UK payroll, the basic calculation process, and common challenges companies face when managing payroll internally.

What Should You Know About Monthly Payroll in the UK?

Monthly payroll is a pay structure in which employees receive their salary once per month on a fixed pay date. This payroll schedule is widely used for salaried employees because it aligns with standard employment contracts and simplifies payroll administration.

In the United Kingdom, employers must process payroll under the Pay As You Earn (PAYE) system. PAYE requires employers to deduct income tax and National Insurance contributions directly from employee wages before the salary is paid. These deductions must then be reported to HMRC through the Real Time Information (RTI) system each time payroll is processed.

Understanding the structure of the monthly payroll is only the starting point. To calculate employee pay accurately, employers must also identify the specific components that make up payroll calculations.

What Components Are Included in Monthly Payroll?

Before calculating payroll, businesses must understand the elements that contribute to an employee’s total pay. Monthly payroll calculations combine multiple components that determine both gross earnings and the final net salary paid to employees.

1. Gross Pay

Gross pay represents the total earnings an employee receives before any deductions are applied. For salaried employees paid monthly, gross pay is typically their fixed monthly salary as stated in their employment contract.

However, gross pay may also include additional earnings that occur during the payroll period. These must be added before any payroll taxes or deductions are calculated.

2. Overtime and Additional Earnings

Many employees receive earnings beyond their standard salary. These additional payments may vary from month to month and must be included in the payroll calculation process.

Common types of additional earnings include:

- Overtime payments for hours worked beyond the standard schedule

- Performance bonuses or commission payments

- Shift allowances or special duty pay

- Holiday pay adjustments

These payments increase the employee’s gross earnings for that payroll period.

3. Payroll Taxes (Income Tax and National Insurance)

Employers are responsible for deducting payroll taxes from employee earnings through the PAYE system. The two primary payroll taxes are income tax and National Insurance contributions.

Income tax deductions depend on the employee’s tax code and total taxable income. National Insurance contributions are calculated based on earnings thresholds and contribute to the UK’s social security system.

Both taxes must be calculated accurately and submitted to HMRC as part of the employer’s payroll obligations.

Not sure how to calculate holiday pay for irregular hours? Read our complete guide to get it right.

4. Pension Contributions

Under UK employment law, eligible employees must be automatically enrolled into a workplace pension scheme. Both employers and employees contribute to the pension fund.

Employee pension contributions are deducted directly from payroll, while employers must also contribute a minimum percentage of the employee’s qualifying earnings. These deductions must be reflected accurately in payroll calculations.

5. Other Payroll Deductions

In addition to taxes and pension contributions, employees may have other deductions applied to their payroll. These deductions depend on the employee’s individual circumstances.

Such as:

- Student loan repayments

- Salary sacrifice arrangements

- Child maintenance payments

- Union membership fees

Each deduction must be recorded and applied correctly during payroll processing.

Once these payroll elements are clearly defined, employers can follow a structured process to calculate employee pay from gross earnings through to the final net salary.

How to Calculate Monthly Payroll?

Calculating payroll requires a structured approach that accounts for earnings, statutory deductions, and employee-specific adjustments. Following a consistent process helps ensure payroll accuracy and compliance.

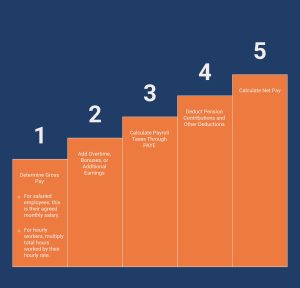

Step 1: Determine Gross Pay

The first step is to identify the employee’s base salary or hourly wage for the payroll period. For salaried employees on a monthly payroll, this usually represents their agreed monthly salary.

For hourly workers, employers must calculate the total number of hours worked during the payroll period and multiply that total by the agreed-upon hourly rate.

Step 2: Add Overtime, Bonuses, or Additional Earnings

Once the base salary is determined, any additional earnings must be included. These may include overtime payments, performance bonuses, commission earnings, or allowances.

Adding these payments ensures that the employee’s total gross earnings for the payroll period are calculated accurately before deductions are applied.

Step 3: Calculate Payroll Taxes Through PAYE

After determining total earnings, employers must apply PAYE tax calculations. Payroll systems use the employee’s tax code and earnings level to determine the correct income tax and National Insurance deductions.

These deductions must be recorded and submitted to HMRC as part of the payroll reporting process.

Step 4: Deduct Pension Contributions and Other Deductions

Next, employee pension contributions are deducted in accordance with workplace pension rules. Additional deductions, such as student loan repayments or salary sacrifice arrangements, are also applied at this stage.

Each deduction must be documented clearly in payroll records to ensure accurate reporting.

Step 5: Calculate Net Pay

The final step is to calculate the employee’s net pay, which is the salary the employee receives after all payroll deductions have been applied.

This net amount is transferred to the employee on the scheduled payroll payment date.

To understand how these steps work in practice, it helps to review a simple payroll calculation example that illustrates how earnings and deductions interact within a monthly payroll cycle.

What Does a Monthly Payroll Calculation Example Look Like?

Understanding payroll calculations becomes easier when you look at a practical example. The scenario below shows how an employee’s gross salary, additional earnings, and statutory deductions combine to determine the final net pay for a monthly payroll cycle.

Consider an employee who receives a fixed monthly salary but also earns overtime during the payroll period.

Step-by-Step Payroll Example

| Payroll Calculation Step | Component | Amount (£) |

|---|---|---|

| Gross Earnings | Base Monthly Salary | 3,000 |

| Overtime Payment | 200 | |

| Total Gross Earnings | 3,200 | |

| Statutory & Payroll Deductions | Income Tax Deduction | 420 |

| National Insurance Contribution | 210 | |

| Workplace Pension Contribution | 96 | |

| Total Deductions | 726 | |

| Net Pay | Final Net Pay (Take-Home Pay) | 2,474 |

Note: The income tax and National Insurance figures shown above are simplified estimates used only for illustration. In practice, deductions depend on several factors, including an employee’s tax code, National Insurance thresholds, pension arrangements, and other payroll adjustments.

How Are Monthly Payroll Taxes Calculated in the UK?

Payroll taxes are calculated automatically through the PAYE system. Employers must apply the correct deductions based on employee income levels, tax codes, and statutory thresholds.

1. Income Tax Bands

The UK income tax system uses progressive tax bands, meaning higher earnings are taxed at higher rates. Payroll software calculates deductions automatically through PAYE based on the employee’s tax code and applicable thresholds. Accurate tax codes are essential so the correct tax bands are applied during payroll calculations.

2. National Insurance Contributions

National Insurance (NI) contributions are mandatory payroll deductions that help fund benefits such as the NHS and State Pension. Employee contributions apply to earnings within specific thresholds, mainly between the Primary Threshold and Upper Earnings Limit. Since NI rates and limits can change each tax year, payroll systems must be updated regularly.

3. Student Loan Deductions

Student loan repayments begin once an employee’s earnings exceed the repayment threshold for their loan plan. The deduction is calculated as a percentage of income above that threshold and processed through PAYE. HMRC notifies employers when deductions should start and which repayment plan applies.

4. Workplace Pension Contributions

Workplace pension contributions are managed through payroll under the UK’s auto-enrolment system. Eligible employees must be enrolled in a pension scheme with both employer and employee contributions. Minimum contributions are calculated as a percentage of qualifying earnings, which fall within government-set earnings thresholds reviewed periodically.

Beyond standard deductions, payroll calculations can also change when employee circumstances shift, requiring additional adjustments during the payroll process.

How Do Payroll Adjustments Affect Monthly Payroll?

Payroll is rarely the same from one month to the next. Various payroll adjustments are often needed to account for changes like new starters, leavers, or periods of absence.

These adjustments can affect everything from gross pay to the final net pay and require careful handling by the HR department to ensure accuracy.

1. Calculating Payroll for a Mid-Month Start Date (New Employees)

When a new employee joins partway through a pay period, payroll must calculate salary only from the official start date to the end of that period. This is a specific new starter scenario in which pay is prorated using a daily rate based on working days and applied only to days worked after joining.

2. Calculating Prorated Payroll for Leavers or Partial Periods

Prorated payroll applies more broadly to situations where pay must be adjusted for only part of a pay period, most commonly when an employee leaves mid-cycle. In these cases, payroll calculates a daily rate and applies it to the employee’s final working days to ensure accurate final pay.

3. Handling Overtime Payments

Overtime applies when employees work beyond their contracted hours and must be calculated separately during payroll processing. Payroll teams determine the employee’s standard hourly rate and apply the agreed-upon overtime rate, often 1.5 times the regular rate, based on the number of additional hours worked in the pay period.

4. Payroll Adjustments for Leave or Absence

Payroll adjustments are required when employees take leave or are absent during a pay period. Paid leave usually maintains normal salary payments in accordance with company policy. In contrast, unpaid leave typically requires a deduction calculated by multiplying the employee’s daily pay rate by the number of absence days.

Alongside these adjustments, the payroll schedule a business chooses can also influence how salaries, overtime, and deductions are calculated throughout the year.

How Do Different Payroll Schedules Affect Payroll Calculations?

The frequency of your payroll schedule directly affects how you perform payroll calculations. The most common payroll schedules in the UK are monthly, semimonthly, and bi-weekly payroll.

Each schedule determines how many pay periods there are in a year, which in turn affects how gross pay and deductions are calculated for each pay period:

1. Monthly Payroll

Monthly payroll pays employees once per month, resulting in 12 pay periods per year. Gross pay is calculated by dividing annual salary by 12, with payroll adjustments such as overtime added and unpaid leave deducted before applying income tax and National Insurance.

2. Semimonthly Payroll

Semimonthly payroll pays employees twice per month, typically on fixed dates such as the 15th and the month-end, resulting in 24 pay periods per year. Because pay periods vary in length, payroll calculations often require prorating salary and adjusting for overtime or leave based on actual days worked.

3. Bi-Weekly Payroll

Bi-weekly payroll pays employees every two weeks on a fixed day, resulting in 26 pay periods per year. Pay is calculated based on hours worked within each period, with overtime and deductions applied consistently due to the fixed two-week structure.

Each pay period always contains two full workweeks, which simplifies calculations compared to a semimonthly schedule. Despite these structured payroll schedules, many organisations still encounter operational challenges.

What Payroll Challenges Do Businesses Face When Calculating Payroll?

Despite the best intentions, businesses often face several payroll challenges when calculating pay. These can range from managing complex pay structures to ensuring compliance with ever-changing tax laws.

These issues can create a significant administrative burden for the HR department and increase the risk of errors:

1. Managing Multiple Pay Structures

Businesses often operate multiple pay structures, such as salaried, hourly, and commission-based models. This creates complexity as each structure requires different payroll rules and calculations. Payroll teams must apply the correct method for each employee, ensuring gross pay, overtime eligibility, and earnings are calculated accurately.

2. Overtime and Variable Pay Calculations

Overtime and variable pay include fluctuating earnings such as extra hours, bonuses, and commissions. The challenge lies in tracking accurate inputs, which can vary from one pay period to the next. Payroll teams must calculate and apply these additions correctly to ensure total earnings reflect actual work and performance.

3. Payroll Tax Compliance and HMRC Reporting

Payroll must comply with HMRC regulations, including correct tax codes, rates, and reporting requirements. The challenge is keeping up with frequent changes in tax rules and thresholds. Payroll teams must calculate statutory deductions accurately and submit PAYE data on time to avoid penalties.

4. Payroll Adjustments and Employee Changes

Employee changes, such as new hires, leavers, and salary updates, require ongoing payroll adjustments. These changes can affect pay, deductions, and entitlements within a pay period. Payroll teams must recalculate figures promptly to ensure all payments remain accurate and compliant.

5. Administrative Workload and Risk of Errors

Payroll processing can involve a significant administrative workload, particularly when handled manually. This increases the risk of errors in data entry, calculations, and compliance updates. Payroll teams must maintain accuracy across all inputs to prevent incorrect pay and potential regulatory issues.

Because of these complexities, many organisations explore external payroll support to help manage calculations, reporting obligations, and compliance requirements more efficiently.

How Directly Payroll Services Simplify Monthly Payroll Calculations?

For many organisations, managing payroll calculations internally can become increasingly complex as employee numbers grow and payroll structures diversify.

Professional payroll providers such as Direct Payroll Services support businesses by managing payroll processing, PAYE calculations, pension contributions, and HMRC reporting, delivering fully managed payroll solutions with dedicated support and real-time reporting for complete visibility and control.

Outsourcing payroll allows businesses to reduce administrative workload while ensuring payroll calculations remain accurate and compliant with UK employment and tax regulations,s with scalable services designed to adapt as your workforce and payroll requirements evolve. This enables employers to focus on operational priorities while maintaining reliable payroll management.

Looking for dependable payroll support? Get in touch with Direct Payroll Services today.

Conclusion

Calculating monthly payroll for UK employees involves multiple steps, from determining gross earnings to applying payroll taxes, pension contributions, and other deductions. Employers must also comply with PAYE regulations and HMRC reporting requirements, making payroll management an important operational responsibility.

As businesses expand and payroll structures become more complex, maintaining payroll accuracy and compliance can require significant time and expertise. Establishing a structured payroll process or working with experienced payroll professionals can help organisations ensure employees are paid correctly while maintaining full compliance with UK payroll regulations.

Frequently Asked Questions

How is overtime calculated on a semimonthly payroll in the UK?

Overtime in a semimonthly pay period is calculated by tracking hours worked beyond the employee’s workweek, typically Monday to Friday. When periods are split, employee hours and overtime hours are accurately divided and added to regular pay.

Are there special UK rules for calculating payroll deductions each month?

Yes, UK payroll deductions are based on taxable pay, employee’s annual salary, and the number of pay periods within the tax year starting in April. Deductions such as health insurance and PAYE must be calculated accurately for each semimonthly pay period.

What’s the difference between gross pay and net pay in payroll?

Gross pay includes regular pay, overtime hours, and earnings based on employee hours and the number of days worked. Net pay is the final taxable pay after deductions like health insurance, calculated from the employee’s annual salary and pay structure.

What is the difference between semimonthly payroll and monthly payroll when it comes to overtime calculation?

Monthly payroll calculates overtime hours for a single cycle, whereas a semimonthly pay period may split the employee’s workweek. This requires carefully allocating overtime hours and employee hours across multiple pay periods to ensure accuracy.

Is an online calculator reliable for figuring out overtime pay on a semimonthly payroll?

An online calculator can estimate overtime hours, but may not reflect real scenarios, such as a split employee’s workweek from Monday to Friday. For accurate calculations of taxable and regular pay, businesses should verify the results using payroll systems.

Are there common mistakes to avoid when calculating overtime for semimonthly payrolls?

Common mistakes include miscounting overtime hours, ignoring the number of days worked, and incorrectly splitting employee hours across a semimonthly pay period. Errors in employees’ annual salary calculations can also impact taxable pay and payroll accuracy.

What are the key steps for manually checking overtime calculations in a semimonthly pay cycle?

Review employee hours, confirm the number of overtime hours, and align them with the employee’s workweek (Monday to Friday). Cross-check regular pay, taxable pay, and the number of days within each semimonthly pay period to ensure accurate results.