Key Highlights

- CIS payroll helps contractors manage subcontractor payments, tax deductions, and HMRC reporting under the Construction Industry Scheme.

- Contractors must verify subcontractors with HMRC before applying CIS deduction rates to payments.

- Registered subcontractors are usually taxed at 20%, while unregistered subcontractors are taxed at 30%.

- CIS payroll differs from PAYE payroll in worker classification, deduction handling, and reporting requirements.

- Incorrect CIS deductions or late monthly returns can lead to HMRC penalties and subcontractor disputes.

- Construction businesses often manage both CIS and PAYE payroll together when handling mixed workforces.

- CIS payroll software automates verification, deductions, and reporting.

- Outsourced CIS payroll services can reduce administrative workload and improve payroll compliance accuracy.

Construction payroll mistakes can quickly create HMRC penalties, delayed payments, and subcontractor disputes. Contractors must accurately manage CIS deductions, worker verification, and monthly reporting while handling multiple projects and fluctuating workforce demands.

Many businesses only realise the complexity of CIS payroll after deduction errors, incorrect worker classification, or late HMRC submissions start affecting operations. Managing both CIS and PAYE payroll together can also increase reporting pressure for construction businesses with mixed workforces.

Understanding how CIS payroll works is important for reducing compliance risks and maintaining accurate payroll processes. This guide explains the Construction Industry Scheme, how CIS payroll differs from PAYE, the responsibilities contractors must manage, and how businesses can improve payroll reporting accuracy.

What is the Construction Industry Scheme (CIS)?

The Construction Industry Scheme (CIS) is an HMRC tax scheme that requires contractors to deduct tax from subcontractor payments and submit those deductions to HMRC. The scheme mainly applies to construction businesses hiring subcontractors for building and construction work.

| Subcontractor Status | CIS Deduction Rate |

|---|---|

| Registered subcontractor | 20% |

| Unregistered subcontractor | 30% |

| Gross Payment Status | 0% |

CIS applies to most construction-related work, including building, repairs, renovations, demolition, decorating, and site preparation. The scheme helps HMRC monitor subcontractor tax reporting and reduce incorrect tax deductions across the construction industry.

How CIS Payroll Differs From Standard Payroll

CIS Payroll is used by contractors to manage payments to subcontractors working under the Construction Industry Scheme. Unlike PAYE payroll, CIS applies specific tax-deduction rules to subcontractor payments in the construction industry.

| Feature | CIS Payroll | PAYE Payroll |

|---|---|---|

| Worker Type | Subcontractors | Employees |

| Tax Deductions | CIS deductions | Income Tax and NICs |

| Reporting | Monthly CIS returns | RTI payroll reporting |

| Payment Documents | CIS deduction statements | Payslips |

| Industry Use | Construction industry | All industries |

Under PAYE payroll, employers deduct Income Tax and National Insurance directly from employee wages. Under CIS payroll, contractors deduct a percentage from subcontractor payments and submit those deductions to HMRC through monthly CIS returns.

How Does Payroll CIS Work?

CIS payroll works by verifying subcontractors, applying the correct CIS deduction rates, submitting monthly returns to HMRC, and maintaining accurate payment records. Contractors are responsible for reporting deductions correctly and ensuring subcontractor payments comply with Construction Industry Scheme rules.

1. Registering for CIS

Contractors hiring subcontractors for construction work must register for CIS with HMRC before processing payments. Subcontractors can also register to reduce their deduction rate from 30% to 20%, while some may qualify for Gross Payment Status with no deductions applied.

2. Verifying Subcontractors and Applying CIS Deductions

Before payments are processed, contractors must verify subcontractors with HMRC to confirm the correct deduction rate.

Standard CIS deduction rates include:

| Subcontractor Status | Deduction Rate |

|---|---|

| Registered subcontractor | 20% |

| Unregistered subcontractor | 30% |

| Gross Payment Status | 0% |

Contractors deduct tax from subcontractor payments and send those deductions directly to HMRC through the CIS system. Incorrect verification or deduction rates can lead to payroll disputes and HMRC compliance issues.

3. Filing Monthly CIS Returns

Contractors must submit CIS returns to HMRC every month, usually by the 19th of the following tax month. Returns must include subcontractor payments, CIS deductions, and verification details.

After deductions are applied, contractors pay subcontractors the remaining balance and issue CIS deduction statements showing:

- gross payment amount

- CIS deductions

- net payment value

Accurate deduction statements help subcontractors track tax payments and maintain clearer records for Self Assessment reporting.

4. Maintaining CIS Payroll Compliance

CIS payroll requires ongoing monitoring to ensure deductions, verification checks, and HMRC reporting remain accurate throughout the year.

Construction businesses managing multiple subcontractors often use CIS payroll software or outsourced CIS payroll services to:

- automate deductions

- manage payroll records

- Submit CIS returns

- reduce manual reporting errors

Consistent payroll processes help contractors avoid HMRC penalties while maintaining more accurate subcontractor payment records. If you’re looking for construction payroll services and wish to learn more, read this blog to Explore Various Types of Construction Payroll Services.

Who Is CIS Payroll Really For and How Does It Affect You?

CIS payroll applies to contractors, subcontractors, and agencies involved in construction work under the Construction Industry Scheme. Contractors managing subcontractor payments must comply with CIS deduction and reporting rules, while agencies supplying construction workers may also have CIS payroll responsibilities, depending on worker classification.

1. Contractors

Contractors hire subcontractors to carry out construction work and are responsible for applying CIS deduction rules correctly. Businesses spending more than £3 million on construction work over three years may also need to register as contractors under CIS.

Contractors must:

- Apply correct CIS deduction rates

- Submit monthly CIS returns

- Maintain accurate payroll records

Many contractors use CIS payroll companies, such as Direct Payroll UK, to handle this for them, ensuring deductions, reports, and HMRC payments are processed correctly.

2. Subcontractors

Subcontractors are self-employed workers or businesses carrying out construction work for contractors. Payments are usually made after CIS deductions are applied unless the subcontractor qualifies for Gross Payment Status.

Registered subcontractors are normally taxed at 20%, while unregistered subcontractors are taxed at 30%.

3. Employment Agencies

Employment agencies supplying workers to construction projects may also have CIS responsibilities depending on worker classification and payment arrangements.

Agencies must determine whether workers fall under PAYE or CIS rules to avoid payroll reporting errors and HMRC compliance issues.

Clear worker classification and accurate payroll processing help agencies avoid compliance risks while managing temporary and project-based construction workers more effectively. If you need to understand the workings of payroll companies, read this blog.

What Is the Difference Between CIS and PAYE Payroll?

Construction businesses often manage both employees and subcontractors, but CIS and PAYE payroll follow different tax and reporting rules. Incorrect worker classification can lead to deduction errors, payroll disputes, and HMRC compliance problems, particularly for businesses managing mixed workforces.

| Feature | CIS Payroll | PAYE Payroll |

|---|---|---|

| Worker Type | Subcontractors | Employees |

| Tax Deductions | CIS deductions | Income Tax and NICs |

| Reporting | Monthly CIS returns | RTI payroll reporting |

| Payment Documents | CIS deduction statements | Payslips |

| Industry Use | Construction industry | All industries |

CIS payroll applies to subcontractors working in construction, while PAYE payroll applies to employees receiving regular wages or salaries. Under PAYE, employers deduct Income Tax and National Insurance directly from employee pay. Under CIS payroll, contractors deduct a percentage from subcontractor payments and report those deductions to HMRC through monthly CIS returns.

1. Can Businesses Run CIS and PAYE Payroll Together?

Many construction businesses manage both CIS and PAYE payroll simultaneously because they employ staff while also hiring subcontractors for project-based work. Office employees, site managers, and permanent workers are usually paid through PAYE, while subcontractors are paid through CIS.

Running both systems together requires accurate worker classification, separate deduction handling, and consistent payroll reporting to HMRC. Incorrectly placing workers under CIS or PAYE can create compliance risks and reporting issues.

2. Do Businesses Need Separate Payroll for CIS?

Businesses do not always need completely separate payroll systems for CIS and PAYE, but they must manage both processes correctly. Many payroll software platforms support combined CIS and PAYE payroll management within a single system.

However, CIS payroll still requires separate subcontractor verification, deduction calculations, monthly CIS returns, and deduction statements. Businesses managing large subcontractor workforces often use specialist CIS payroll services or software to reduce reporting errors and administrative pressure.

What Responsibilities Do Contractors Have Under CIS Payroll?

Contractors managing CIS payroll must apply the correct deduction rates, maintain accurate payroll records, and submit monthly CIS returns to HMRC. Incorrect deductions or incomplete records can quickly create unpaid tax liabilities, reporting issues, and subcontractor disputes.

1. Calculating Accurate CIS Deductions

Contractors must apply CIS deductions based on each subcontractor’s HMRC verification status. Registered subcontractors are usually taxed at 20%, while unregistered subcontractors are taxed at 30%.

For example, applying a 20% deduction instead of 30% for an unverified subcontractor can leave contractors liable for unpaid tax.

Before processing payments, contractors should confirm:

- Subcontractor verification status

- correct deduction rates

- labour costs excluding VAT

- gross payment status eligibility

2. Keeping Payroll Records Compliant

Contractors must maintain accurate records of subcontractor payments, CIS deductions, verification checks, and monthly CIS returns. HMRC may request these records during compliance reviews or investigations.

Important CIS payroll records include:

- Subcontractor verification details

- CIS deduction statements

- Payment records

- Monthly CIS return submissions

- HMRC correspondence

Consistent recordkeeping helps contractors reduce reporting errors and respond more efficiently to HMRC queries.

3. Communicating Deductions Clearly to Subcontractors

Contractors must provide subcontractors with clear CIS deduction statements showing payment amounts, deductions applied, and verification details. Poor communication around deductions often leads to disputes, payment confusion, and reconciliation issues at the end of the tax year.

Clear reporting helps subcontractors:

- track deductions accurately

- prepare tax returns

- Identify deduction errors early

- maintain their own financial records

Providing accurate deduction information also helps contractors maintain stronger working relationships with subcontractors across ongoing construction projects.

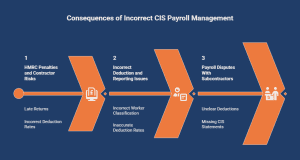

What Happens If CIS Payroll Is Managed Incorrectly?

Incorrect CIS payroll can create more than HMRC reporting problems. Late returns, incorrect deduction rates, or poor worker classification can delay payments, disrupt project timelines, and damage subcontractor relationships across construction projects.

| CIS Payroll Error | Potential Consequence |

|---|---|

| Incorrect deduction rates | Unpaid tax liabilities and subcontractor disputes |

| Late CIS returns | HMRC penalties starting from £100 |

| Incorrect worker classification | PAYE and CIS tax investigations |

| Poor payroll records | Delayed HMRC audits and reporting issues |

| Missing deduction statements | Payment disputes and reconciliation problems |

1. HMRC Penalties and Contractor Risks

HMRC can issue penalties when contractors submit late CIS returns, apply incorrect deduction rates, or fail to maintain accurate payroll records.

For example, applying a 20% deduction instead of 30% for an unverified subcontractor can leave contractors liable for unpaid tax. Repeated reporting failures may also trigger HMRC investigations or compliance reviews.

Beyond financial penalties, payroll errors can create:

- delayed subcontractor payments

- project administration issues

- additional accounting costs

- internal payroll pressure

2. Incorrect Deduction and Reporting Issues

Incorrect CIS deductions can create cash flow strain for subcontractors and unexpected tax liabilities for contractors. Even small payroll mistakes can become larger reporting problems when businesses manage multiple subcontractors across different projects.

Reporting problems commonly occur when:

- workers are classified incorrectly

- Deduction rates are applied inaccurately

- Payments are processed before verification

- CIS returns contain incomplete information

Inconsistent payroll records can also delay tax reconciliation and create administrative pressure during HMRC reviews.

3. Payroll Disputes With Subcontractors

Unclear deductions, missing CIS statements, or inaccurate payment records can quickly damage subcontractor trust. Construction projects often depend on reliable subcontractor relationships, making payroll accuracy critical for ongoing operations.

For example, delayed deduction statements or unexplained payment reductions can lead to disputes over outstanding balances and project delays.

Clear payroll communication helps businesses:

- reduce payment disputes

- maintain subcontractor confidence

- avoid reconciliation issues

- improve payment transparency

Clear communication and accurate payroll reporting help contractors reduce disputes while maintaining more reliable working relationships across construction projects.

What Should Businesses Look for in CIS Payroll Software?

Choosing the wrong CIS payroll software can create reporting delays, deduction mistakes, and unnecessary admin pressure, especially for construction businesses managing multiple subcontractors. The best CIS payroll software should simplify HMRC reporting, reduce manual calculations, and support both CIS and PAYE payroll within one system.

| Feature | Why It Matters |

|---|---|

| HMRC subcontractor verification | Reduces incorrect deduction rates |

| Automated CIS deductions | Minimises manual payroll errors |

| CIS return submissions | Helps avoid late filing penalties |

| Combined CIS and PAYE payroll | Simplifies mixed workforce management |

| Payroll reporting tools | Improves payment tracking and records |

1. Must-Have CIS Payroll Software Features

Construction businesses often benefit from software that can:

- automate CIS deductions

- generate CIS deduction statements

- track subcontractor payment history

- store payroll records centrally

- Submit monthly CIS returns directly to HMRC

For example, businesses managing subcontractors across multiple projects may struggle with manual spreadsheets, delayed reporting, or inconsistent deduction records without automated payroll tools.

2. Red Flags to Avoid

Some payroll systems create more administration rather than reducing it. Businesses should avoid CIS payroll software that:

- Lacks HMRC verification integration

- requires manual deduction calculations

- separates CIS and PAYE reporting unnecessarily

- offers limited payroll reporting visibility

- Makes CIS return submissions difficult

Poor payroll systems can increase reporting errors and make HMRC audits harder to manage.

3. Managing CIS and PAYE Payroll Together

Many construction businesses employ office staff under PAYE while paying subcontractors through CIS. Using separate payroll systems for each workforce can create duplicate reporting tasks and inconsistent records.

Integrated CIS and PAYE payroll software helps businesses:

- Manage employee and subcontractor payments together

- maintain separate deduction rules

- improve payroll visibility

- reduce administrative workload

This is particularly useful for growing construction businesses handling multiple projects and mixed workforce structures.

How Can Direct Payroll Services Support CIS Payroll Management?

Managing CIS payroll internally can become difficult when contractors handle multiple subcontractors, ongoing HMRC reporting requirements, and mixed CIS and PAYE workforces. Incorrect deductions, delayed submissions, or inconsistent payroll records can quickly create compliance risks and subcontractor disputes, especially when considering the VAT reverse charge rules.

Direct Payroll Services supports construction businesses with CIS payroll management, subcontractor verification, deduction processing, payroll reporting, and HMRC submissions. The service helps contractors manage payroll responsibilities more accurately while reducing administrative workload across construction projects.

Direct Payroll Services can support businesses with:

- subcontractor verification checks

- CIS deduction calculations

- Monthly CIS return submissions

- CIS deduction statements

- Payroll record management

- Combined CIS and PAYE payroll support

Construction businesses managing growing subcontractor workforces often need more structured payroll processes to maintain reporting accuracy and avoid HMRC penalties. Outsourced CIS payroll support can help contractors reduce manual administration while improving payroll consistency across multiple projects.

Businesses looking to simplify CIS payroll management and improve payroll compliance can explore Direct Payroll Services CIS payroll support for additional guidance and payroll assistance.

Conclusion

Managing CIS payroll requires contractors to handle subcontractor verification, deduction calculations, monthly CIS returns, and payroll recordkeeping accurately, while ensuring that National Insurance contributions are also considered. Incorrect deductions, late reporting, or poor worker classification can quickly create HMRC compliance issues, financial penalties, and subcontractor disputes across construction projects.

Understanding how CIS payroll works, how it differs from PAYE payroll, and what responsibilities contractors must manage in relation to the amount of tax can help construction businesses improve payroll accuracy and reduce reporting risks. Many businesses also use CIS payroll software or outsourced payroll support to simplify payroll administration and maintain more consistent HMRC reporting processes.

Frequently Asked Questions

How does CIS payroll work for contractors and subcontractors?

CIS payroll works by verifying subcontractors with HM Revenue and Customs (HMRC), applying the correct CIS deduction rates to payments, and submitting monthly CIS returns, including domestic reverse charge aspects. Contractors manage deductions and reporting, while subcontractors receive payments after HM revenue tax deductions are applied.

What steps do I need to follow to set up CIS payroll for my construction business?

To set up CIS payroll, construction businesses must register for CIS with HMRC, verify CIS subcontractors at construction sites before payments are made, apply the correct deduction rates, maintain payroll records, and submit monthly CIS returns. Many businesses also use CIS payroll software or outsourced payroll services to manage reporting accurately.

Are there any specific payroll software options designed for CIS compliance?

Yes, several payroll software systems are designed for CIS compliance. They can automate subcontractor verification, CIS deductions, monthly HMRC returns, payroll reporting, and combined CIS and PAYE payroll management for construction businesses.

What are the key legal requirements under the Construction Industry Scheme for payroll?

Key legal requirements under CIS include registering with HMRC, verifying subcontractors before payment using their unique taxpayer reference, applying the correct deduction rates, submitting monthly CIS returns, issuing deduction statements, and maintaining accurate payroll records to support HMRC compliance and reporting obligations.

Can sole traders use CIS payroll services, or is it only for larger businesses?

Yes, sole traders can use CIS payroll services. Many sole traders working as contractors or subcontractors use CIS payroll support to manage deductions, HMRC reporting, verification checks, and tax treatment payroll records more accurately, especially when handling multiple construction projects or subcontractor payments.

How does CIS impact tax deductions for construction workers?

CIS impacts tax deductions by requiring contractors, including property developers, to deduct tax directly from subcontractor payments before they are paid. Registered subcontractors are usually taxed at 20%, while unregistered workers are taxed at 30% under HMRC Construction Industry Scheme rules.

Where can I find official guidance about CIS payroll from the UK government?

Official CIS payroll guidance is available through the UK Government and HMRC websites. Businesses can find information about CIS registration, tax affairs, deduction rates, subcontractor verification, and monthly CIS returns on the HMRC Construction Industry Scheme guidance.