TL;DR

|

|---|

Many people dread tax season, wondering: “How can I save more without feeling the pinch each month?” Salary sacrifice could be the answer. It lets you reduce your taxable pay in exchange for benefits, like pension boosts, electric vehicle leasing, etc. So you keep more of your earnings.

In this post, we’ll show you exactly how salary sacrifice works in 2025, the real savings you can expect, and the risks to watch out for, especially for low earners or those planning big financial moves like a mortgage. By the end, you’ll know whether this setup could work in your favour (or not)

What Is Salary Sacrifice UK?

Have you ever heard of salary sacrifice but weren’t quite sure what it meant? Simply put, it’s an arrangement between you and your employer where you agree to give up a portion of your salary in return for a non-cash employee benefit.

This isn’t just an informal agreement; it involves a formal change to your employment contract. The amount of salary you exchange is deducted from your gross pay before any taxes are calculated.

How Does Salary Sacrifice Work in 2025?

Entering into a salary sacrifice arrangement in the 2025 tax year is an easy process. The following sections will explore exactly how this process unfolds and why it’s becoming an increasingly popular choice for employees and employers alike.

Understand pre-tax deductions in the UK with this detailed guide.

1. Reducing Gross Salary Before Tax

What happens with salary sacrifice is simple: it reduces your gross salary before tax is applied. This arrangement, sometimes called a salary exchange, is a formal change in your employee’s contract. You agree to receive a lower salary, and your employer provides a benefit to make up for the difference.

So, does this affect your take-home pay and taxes? Absolutely. By lowering your gross salary, you immediately reduce the amount of take-home pay and tax you owe to HMRC.

2. Employer and Employee Contributions

When it comes to pensions, salary sacrifice eases how contributions are made. Instead of making employee contributions from your post-tax pay, you sacrifice a portion of your pre-tax salary. Your employer then pays this amount directly into your pension scheme on your behalf.

Salary sacrifice is one of the most tax-efficient ways to contribute to your pension. With Salary Sacrifice pension tax relief, your contributions are taken before tax, helping you save on both Income Tax and National Insurance while your pension pot grows faster.

This means the full amount you sacrifice goes into your pension, along with the standard employer pension contribution. Some employers even pass on their National Insurance savings by adding more to their pension pot.

3. Salary Sacrifice HMRC Warning

HMRC requires strict compliance. Schemes must not reduce salaries below the National Minimum Wage, and benefits must be set out in a formal written agreement. Getting it wrong can trigger penalties.

Why Is Salary Sacrifice Gaining Popularity?

The popularity of salary sacrifice is on the rise, and it’s easy to see why. The main advantages of salary sacrifice are the significant financial benefits it offers to both employees and employers.

1. Salary Sacrifice for Employees

For employees, salary sacrifice is a formal contract change, not an informal perk. It lowers taxable income while providing access to benefits like pensions, EV leasing, or tech purchases.

2. Employers Offering Attractive Benefits Packages

In a competitive job market, employers are constantly looking for ways to attract and retain top talent. Offering an attractive employee benefit package is a main part of this, and being able to offer salary sacrifice is a powerful way.

3. Salary Sacrifice Employer Benefits

Even employers receive many benefits by adopting salary sacrifice, as these schemes reduce overall NI liabilities and make benefit packages more appealing. This not only lowers costs but also helps attract and retain top talent.

What Are the Top Benefits of Salary Sacrifice in 2025?

Looking to make your money work smarter in 2025? Salary sacrifice schemes could be exactly what you need. Whether you’re focused on boosting your take-home pay now or building a stronger financial future, these arrangements can really work in your favour.

Stay compliant in 2025 with this detailed guide to the key UK payroll legislation updates.

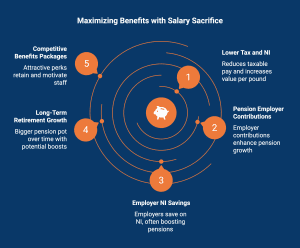

1. Salary Sacrifice to Lower Tax

The core benefit of salary sacrifice is lowering taxable pay. By reducing your gross salary, you immediately pay less in Income Tax and National Insurance, while your chosen benefit increases in value.

2. Salary Sacrifice Pension Employer Contributions

In addition to your own sacrificed salary, your employer continues to add their standard contribution. Some employers even share their NI savings by adding extra to your pension pot.

Here’s how salary sacrifice can boost your pension:

- Your contributions are made before tax, increasing their value.

- It allows you to make larger contributions with a smaller impact on your net pay.

- Some employers add their National Insurance savings to your pension, giving you an extra boost.

3. Salary Sacrifice Employer NI Savings

Employers save on their NI contributions whenever staff join a scheme. Many pass these savings on, boosting employee pensions further.

The most immediate and obvious benefit of salary sacrifice is the savings on tax and National Insurance. When you agree to a lower gross salary, the amount of tax and NI you are required to pay automatically decreases.

The tax implications are simple: your tax is calculated on your reduced salary, so you pay less. For example, an employee earning £30,000 who sacrifices £1,500 for their pension will only be taxed on £28,500.

This applies to both employees and employers. While you save on income tax and NI, your employer saves on their own NI contributions.

4. Long-Term Retirement Growth

Here’s where things get really exciting for your future self. When you combine all these salary sacrifice benefits, your pension pot can grow much faster than you might expect. You’re not just making bigger contributions; you might also benefit from your employer passing on their National Insurance savings to you.

Salary sacrifice only affects your workplace or private pension, not your state pension. Your state pension depends on your National Insurance record, so keep earnings above the Lower Earnings Limit.

5. Offering Competitive Benefits Packages

Want to know the secret to keeping your best employees happy while saving money? It’s all about creating a benefits package that people actually get excited about.

When you offer salary sacrifice arrangements, you’re not just throwing in random perks; you’re giving your team real value through things like childcare vouchers or company cars.

What Are the Disadvantages of Salary Sacrifice UK in 2025?

While salary sacrifice offers many perks, it’s also important to be aware of the potential disadvantages. These schemes are not suitable for everyone, and understanding the trade-offs is key before you commit.

1. Salary Sacrifice on Payslip

Your payslip will reflect a lower gross salary after sacrifice. This means less cash in hand each month, even though your pension contributions rise.

Before opting in, you should consider:

- Your monthly budget and whether you can manage with less cash.

- The actual value of the benefit compared to the reduction in pay.

- How the tax savings will partially offset the lower salary.

Learn how to read your payslip easily with this detailed guide to UK payslip abbreviations.

2. Reduced Gross Salary Leading to Lower Net Income

It’s essential to understand that a reduced gross salary directly results in a lower net income. The core principle of salary sacrifice is exchanging a portion of your pre-tax earnings for a benefit, which means that portion of your pay is no longer available as cash.

Employers have a legal obligation to ensure that the sacrifice does not reduce an employee’s earnings below the National Minimum Wage.

3. Potential Effects on Statutory Benefits

A significant drawback to consider is how salary sacrifice affects your entitlement to certain statutory benefits. Many state benefits, such as Statutory Paternity Pay, are calculated based on your average weekly earnings. A lower gross salary can lead to a lower entitlement.

Potential effects include:

- Reduced Statutory Maternity or Paternity Pay.

- Lower entitlement to some contribution-based state benefits.

- Impacts on life cover or income protection policies that are based on salary.

- It is therefore important to weigh these risks before joining a scheme.

4. Lower Reported Income Affecting Borrowing Capacity

The lower reported income that results from salary sacrifice can be a significant hurdle when seeking credit. A lower income means a lower borrowing limit.

For example, if a lender offers a mortgage of 4.5 times your salary, a £2,000 reduction in your gross pay could reduce your potential mortgage by £9,000. This is a critical factor for anyone in the salary sacrifice worker group who is also looking to buy a home.

Before you join a scheme, it is essential to consider your future financial plans. If a mortgage or large loan is on the horizon, the impact on your reported income and borrowing capacity might outweigh the tax benefits of the scheme.

Discover why payroll is crucial for every UK business in our detailed guide.

5. Administrative Challenges for Employers

Setting up salary sacrifice can create some real administrative headaches for employers. You’ll need meticulous record-keeping to ensure employee contributions match their contracts and stay compliant with HMRC regulations.

Your payroll system will need updates to handle changes in taxable income, National Insurance, and pension contributions, and that takes time. Plus, your HR team needs training to manage these complexities effectively.

6. Complexity in Managing Multiple Benefit Schemes

Running multiple salary sacrifice schemes can quickly become a headache for employers. Each benefit, pensions, company cars, tech equipment, has different rules, tax implications, and compliance requirements.

Get something wrong, and you could face HMRC penalties or employee disputes.

The main challenges include:

- Keeping track of different rules for different benefits

- Ensuring correct payroll deductions for each scheme

- Staying up-to-date with changing legislation that affects each benefit.

What Are Common Salary Sacrifice Schemes in 2025?

There are many popular salary sacrifice schemes available in 2025 that allow employees to exchange part of their salary for a benefit. The most common is for workplace pension contributions, but options have expanded far beyond that.

1. Workplace Pension Contributions

Here’s why salary sacrifice works so well:

- Maximises Pension Contributions: Your full contribution goes into your pension without being reduced by tax or NI.

- Boosts Take-Home Value: For example, contributing £100 means the entire £100 goes into your pension pot.

- Saves Employer Costs: Employers also save on NI, making them more open to offering salary sacrifice schemes.

- Win-Win Outcome: You build a bigger pension, while your employer reduces costs.

To avoid legal risks and penalties, read this detailed guide on why UK employers must issue payslips.

2. Electric Vehicle Leasing Schemes

Electric vehicle leasing schemes are one of the fastest-growing salary sacrifice benefits. Through a salary sacrifice arrangement, you can lease a brand-new electric vehicle for a fixed monthly cost taken directly from your gross salary.

Key features of an EV scheme include:

- Significant savings on income tax and National Insurance.

- No deposit or credit check is typically required.

- It supports a more environmentally friendly commute.

3. Technology and Equipment Schemes

Technology schemes are another popular salary sacrifice option that helps employees acquire the latest gadgets. These equipment schemes allow you to purchase items like laptops, smartphones, or tablets and spread the cost over a year through deductions from your gross salary.

Benefits of technology schemes include:

- Spreading the cost of expensive electronics over manageable monthly payments.

- Saving on NI contributions, effectively giving you a discount on the item.

- No need for credit checks or interest-bearing loans.

Why Choose Direct Payroll Services?

When it comes to providing the best payroll services, Direct Payroll Services makes the process seamless and compliant. We help employers design and implement schemes that are:

- Fully aligned with HMRC rules and ensures deductions never drop salaries below the minimum wage.

- Transparent and easy for staff to understand, reducing admin burden and confusion.

- Tailored to include benefits employees value, like enhanced pension contributions or tax-friendly non-cash perks.

By partnering with Direct Payroll Services, businesses can offer attractive salary sacrifice options that save on National Insurance and payroll taxes, while keeping the scheme clear and compliant. Contact us today!

Conclusion

So there you have it, salary sacrifice can be a real win-win for everyone involved. Whether you’re looking to boost your pension contributions, reduce your tax bill, or create a more attractive benefits package for your team, it’s definitely worth exploring.

Frequently Asked Questions

How can salary sacrifice boost my workplace pension?

Salary sacrifice boosts your workplace pension by allowing you to make additional pension contributions from your pre-tax salary. This means more of your money goes into your pension pot instead of to the tax office, and some employers even top it up with their own NI savings.

Does salary sacrifice affect my take-home pay and tax?

Yes, salary sacrifice reduces your taxable income, which means you pay less income tax and National Insurance. However, because you are agreeing to a lower amount of salary, your monthly cash take-home pay will also be lower, even with the tax savings taken into account.

Is salary sacrifice a good option for small business employers?

For a small business, salary sacrifice can be an effective way to offer competitive benefits and save on employer National Insurance costs. However, employers must ensure their payroll provider can handle the administration and that they have the resources to manage the scheme correctly.

Are there any legal risks or compliance issues with salary sacrifice in the UK?

Yes, there are legal risks. A salary sacrifice is a formal change to an employment contract and a matter of employment law. Employers must follow strict Her Majesty’s Revenue and Customs rules to avoid compliance issues and penalties.

Can salary sacrifice affect my eligibility for certain benefits or loans?

Yes, it can. A lower reported income from salary sacrifice can reduce your entitlement to earnings-related state benefits like Statutory Maternity Pay. It can also negatively impact loan applications, as many lenders base their affordability checks on your new, lower gross salary.

What impact does salary sacrifice have on National Insurance contributions?

Salary sacrifice reduces National Insurance contributions for both employees and employers. This is one of the main National Insurance advantages of the scheme.

How much will it cost my company to set up salary sacrifice?

The direct cost can be minimal, as some providers offer free setup. However, there are indirect costs associated with the administrative challenges of managing a salary sacrifice arrangement.

How can salary sacrifice affect my tax situation and take-home pay?

Salary sacrifice lowers your gross salary, which reduces your taxable income and the amount of tax you pay. While this saves you money on income tax, it also means your cash take-home pay will be lower than before you joined the scheme.

What are the benefits of using salary sacrifice options for employees?

The main advantages of salary sacrifice schemes for employees are the tax savings on income tax and National Insurance. This employee benefit makes it cheaper to pay for things like pensions and cars.

Are there any drawbacks or risks associated with salary sacrifice arrangements?

Yes, the disadvantages of a salary sacrifice arrangement include a lower take-home pay, potential reduction in statutory benefits like maternity pay, and administrative complexity. Unlike a simple net pay arrangement, it can also affect mortgage applications due to a lower reported salary.

How do I calculate my pension contributions with salary sacrifice?

To calculate your pension contributions with salary sacrifice, determine how much of your gross salary you wish to exchange, and that amount will be paid directly into your pension as an employer contribution, rather than being deducted from your payslip.

How do employers set up and manage salary sacrifice arrangements?

They update contracts so employees agree to give up part of their salary for a benefit, ensure the reduced salary stays above the National Minimum Wage, adjust payroll to reflect the change, and maintain accurate records.

What are the potential drawbacks of salary sacrifice schemes?

Reduced gross pay can lower your statutory benefits and borrowing power (like mortgages), reduce life or income protection cover, and for low earners could risk violating income minimums.

What is the difference between salary sacrifice and after-tax contributions?

With salary sacrifice, part of your pay is given up before tax/NI, so you (and the employer) save on those contributions. After-tax contributions are taken after all deductions, so less tax relief.

How does salary sacrifice benefit employer?

Employers pay lower National Insurance contributions because employees’ gross salary is reduced. Also, salary sacrifice schemes can help attract/retain staff through better benefits, improving morale.

Does Salary Sacrifice Cost the Employer?

Generally, no. It saves employers money on NI contributions. However, admin setup, payroll adjustments, and communication with staff can create additional overhead.